Hanza: Softer Market and Integrations Hurting Short-Term

Research Update

2024-05-13

06:45

Analyst Q&A

Closed

Fredrik Nilsson answered 3 questions.

Redeye retains its positive stance towards Hanza despite a softer Q1 report than expected, resulting in lowered forecasts and Base Case. The softer market and the integration of Orbit One are hurting margins somewhat more than we anticipated, reducing our short-term forecasts. On the other hand, management seems very confident in the 2025 targets despite the somewhat softer market.

FN

FR

Fredrik Nilsson

Fredrik Reuterhäll

Contents

Review of Q1 2024

Softer Than Expected

Main Markets

Other Markets

Large Inventory in Orbit One

Estimate Revisions: Reduced Forecasts for 2024 and 2025

Valuation

Investment thesis

Quality Rating

Financials

Rating definitions

The team

Download article

Integrations Hurting Short-Term EBITA

Sales was 6% short of our expectations and amounted to SEK1253m (1065). The organic growth was -6% y/y. The softer macroeconomic environment resulted in lower demand from customers in some areas. EBITA (adjusted for restructuring and a write-down of the Orbit One earn-out) was SEK67m (88), corresponding to an EBITA margin of 5.3% (8.3). Our forecast was SEK96m and 7.2%. Main Markets was only slightly softer than expected, while Other Markets was hurt by a combination of integration work and by having less mature clusters than Main Markets, making it harder to adapt to changes in demand.

Confident in 2025 Targets Despite Somewhat Softer Market

Despite the softer market, management is confident in reaching its 2025 targets of SEK6.5 billion in sales (including future M&A) and an 8% EBITA margin. The company is getting promising signals from its customers, who are expecting to increase their volumes by autumn. Also, management seems confident in gaining new deals during the rest of 2024, thanks to companies continuing to evaluate their production chains, which might be more appealing in a somewhat softer market environment.

New Base Case SEK73 (90)

We lower our Base Case somewhat to SEK 73 (90) on the back of reduced forecasts and a softer outlook. Nevertheless, we keep our positive view and see substantial upside potential. Despite the strong operational performance in recent years, with high growth and improving margins during 2023, Hanza is still trading at a discount to the average, although often bigger, manufacturing service companies. We believe the discount will decrease further, given that Hanza will continue its strong operational performance.

Key financials

| SEKm | 2023 | 2024e | 2025e | 2026e | 2027e |

| Revenues | 4,154.0 | 5,158.2 | 5,611.9 | 5,947.9 | 6,304.1 |

| Revenue Growth | 16.4% | 24.2% | 8.8% | 6.0% | 6.0% |

| EBITDA | 464.7 | 485.0 | 605.4 | 655.6 | 713.0 |

| EBIT | 328.0 | 311.7 | 424.1 | 468.2 | 514.3 |

| EBIT Margin | 7.9% | 6.1% | 7.6% | 7.9% | 8.2% |

| Net Income | 215.0 | 139.6 | 215.3 | 251.9 | 290.2 |

| EV/Sales | 0.9 | 0.6 | 0.5 | 0.5 | 0.4 |

| EV/EBIT | 11.2 | 9.5 | 6.6 | 6.0 | 5.3 |

Review of Q1 2024

| Estmates vs. Actuals | ||||||

| Sales | Q1E 2024 | Q1A 2024 | Diff | Q1A 2023 | Q4A 2023 | |

| Net sales | 1334 | 1253 | -6% | 1065 | 1056 | |

| Y/Y Growth (%) | 33% | 18% | 29% | 5% | ||

| Main Markets | 735 | 770 | 5% | 594 | 605 | |

| Y/Y Growth (%) | 21% | 30% | 23% | 6% | ||

| EBITA (MM) | 61 | 54 | -11% | 58 | 63 | |

| EBITA margin | 8.3% | 7.0% | 10% | 10% | ||

| Other Markets | 599 | 480 | -20% | 468 | 447 | |

| Y/Y Growth (%) | 34% | 3% | 37% | 2% | ||

| EBITA (OM) | 37 | 16 | -56% | 30 | 29 | |

| EBITA margin | 6.1% | 3.3% | 6% | 6% | ||

| Earning | ||||||

| EBITA | 96 | 67 | -30% | 88 | 76 | |

| EBITA Margin (%) | 7.2% | 5.3% | 8.3% | 7.2% | ||

| EBIT | 92 | 61 | -34% | 84 | 71 | |

| EBIT Margin (%) | 6.9% | 4.9% | 7.9% | 6.7% | ||

| Diluted EPS | 1.32 | 0.77 | -42% | 1.48 | 1.09 |

Softer Than Expected

Sales was 6% short of our expectations and amounted to SEK1253m (1065). The organic growth was -6% y/y. The softer macroeconomic environment resulted in lower demand from customers in some areas. EBITA (adjusted for restructuring and a write-down of the Orbit One earn-out) was SEK67m (88), corresponding to an EBITA margin of 5.3% (8.3). Our forecast was SEK96m and 7.2%.

Main Markets beat our sales forecasts by 5%, while EBITA came in 11% short. We believe the EBITA contribution from Orbit One was lower than we anticipated, as management states that the EBITA contribution in Q1 was limited. Thus, the like-for-like EBITA development was rather solid at 8.2% vs 8.8% Q1 2023 (excluding subsidiaries). Organic growth was 1%. Once again, Main Markets shows it has the ability to obtain healthy results despite large integrations and changes in demand.

Other Markets came in below in terms of both sales and EBITA. Organic growth was -14%, and the EBITA margin fell to 3.3% overall and 4.9% (6.4) like-for-like. Our forecast was 6.1%. The growth and margin were negatively affected by the ongoing integration of Orbit One's Polish operations, which usually take one year and could possibly be completed in Q3 if done well. In addition, the smaller clusters within Other Markets are not as mature and, therefore, not as resistant to changes in demand as Main Markets.

Management sees a mixed market where some sectors, like defence and energy, continue to do well, while others like mining and industrials, are softer. Hanza saw lower volumes from some customers while others increased their volume. However, considering the negative organic growth, customers reducing volumes seem to dominate. Also, Hanza has not lost any customers, meaning that the decline in sales is fully due to lower volumes from current customers. Although Hanza plans for the market environment to remain unchanged, it is getting promising signals from its customers, who expect to increase their volumes by autumn.

Also, management highlights that softer macroeconomic conditions can trigger product companies to evaluate their production chains – leaving opportunities for Hanza to gain market share. In addition, the interest in regionalised production remains high, which seems reasonable considering the increasing geopolitical turmoil in many areas, for example. The backsourcing or regionalisation is mostly about new production for the European/American markets being manufactured in those regions rather than production moving back from Asia, although that happens sometimes as well. Management seems confident in gaining new deals thanks to these trends during the rest of 2024.

All in all, management clearly believes that its 2025 targets of SEK6.5bn in sales (inc. future M&A) and the 8% EBITA margin target hold even in this somewhat softer market, suggesting high confidence in reaching the targets.

Source: Hanza

Main Markets

Source: Hanza

Main Markets consist of the Swedish, Finnish, and German clusters. The Swedish cluster is the largest and the most profitable cluster, with manufacturing facilities mainly located in Årjäng and Töcksfors, Värmland, along with the recently acquired facility in Ronneby, Blekinge. The German cluster is less mature but has seen substantial improvements in profitability during the last year. The Finnish cluster is somewhere in between, in terms of maturity and profitability.

Other Markets

Source: Hanza

Other Markets consist of the Baltic, Central European, and Chinese clusters. The Baltic cluster is the largest and likely the most profitable, with manufacturing facilities in Tartu and Narva, Estonia. The Central Europan cluster is less mature but will increase significantly in size with the recently acquired Orbit One factory in Poland. The Chinese cluster is Hanza’s smallest and the only cluster outside of Europe.

Large Inventory in Orbit One

Orbit One has a much larger net working capital compared to “old Hanza”, mostly due to its large inventory. Management believes it will be able to adjust Orbit One’s inventory to align with levels seen previously in Hanza over time, which will boost Hanza’s cash flow.

Source: Hanza

Estimate Revisions: Reduced Forecasts for 2024 and 2025

We lower our sales forecasts by 3-7% for 2024-25 and our EBITA estimates by 14-20%. The following changes mainly drive the revisions in addition to the softer Q1, affecting 2024 numbers:

- While management sees potential for a rebound in volumes in the autumn and has a positive outlook regarding additional deals, the lower activity seen in Hanza and its peers makes us somewhat more cautious regarding our sales expectations. Also, prior to its full integration, we believe the EMS-focused Orbit One is more sensitive to softer economic conditions.

- The lower sales volumes and us likely underestimating the negative margin impact from the integration work result in reduced margin forecasts, mainly for 2024.

Based on our revised forecasts, we expect SEK5.6bn in sales (with no future M&A) and 8.0% in EBITA margin in 2025. This margin is in line with Hanza’s >8% target but somewhat lower sales than the SEK6.5bn target. However, our forecasts do not include any future M&A, and we interpret management as the target is likely to be reached by a combination of organic and acquired growth. Thus, despite our forecast cuts, we still expect Hanza to perform in line with its financial targets.

| Estimate Revisions | ||||||

| Sales | FYE 2024 | Old | Change | FYE 2025 | Old | Change |

| Net sales | 5138 | 5312 | -3.3% | 5600 | 6016 | -6.9% |

| Y/Y Growth (%) | 24% | 28% | 9% | 13% | ||

| Main Markets | 3121 | 2971 | 5.0% | 3401 | 3351 | 1.5% |

| Y/Y Growth (%) | 33% | 26% | 9% | 13% | ||

| EBITA (MM) | 227 | 258 | -11.9% | 299 | 318 | -6.0% |

| EBITA margin | 7% | 9% | 9% | 10% | ||

| Other Markets | 2018 | 2341 | -13.8% | 2199 | 2665 | -17.5% |

| Y/Y Growth (%) | 13% | 32% | 9% | 14% | ||

| EBITA (OM) | 99 | 153 | -35.1% | 154 | 195 | -20.9% |

| EBITA margin | 5% | 7% | 7% | 7% | ||

| Earning | ||||||

| EBITA | 338 | 405 | -16.6% | 447 | 507 | -11.8% |

| EBITA Margin (%) | 6.6% | 7.6% | 8.0% | 8.4% | ||

| EBIT | 312 | 392 | -20.4% | 424 | 495 | -14.3% |

| EBIT Margin (%) | 6.1% | 7.4% | 7.6% | 8.2% | ||

| Diluted EPS | 3.23 | 5.72 | -43.5% | 4.98 | 7.70 | -35.3% |

| Source: Hanza & Redeye Research |

| Forecasts | ||||||||

| Sales | FYA 2023 | Q1A 2024 | Q2E 2024 | Q3E 2024 | Q4E 2024 | FYE 2024 | FYE 2025 | FYE 2026 |

| Net sales | 4144 | 1253 | 1286 | 1249 | 1354 | 5138 | 5600 | 5936 |

| Y/Y Growth (%) | 17% | 18% | 20% | 31% | 28% | 24% | 9% | 6% |

| Main Markets | 2351 | 770 | 788 | 751 | 812 | 3121 | 3401 | 3605 |

| Y/Y Growth (%) | 19% | 30% | 30% | 37% | 34% | 33% | 9% | 6% |

| EBITA (MM) | 256 | 39 | 59 | 60 | 69 | 227 | 299 | 324 |

| EBITA margin | 11% | 5% | 8% | 8% | 9% | 7% | 9% | 9% |

| Other Markets | 1778 | 480 | 498 | 498 | 542 | 2018 | 2199 | 2331 |

| Y/Y Growth (%) | 13% | 3% | 9% | 23% | 21% | 13% | 9% | 6% |

| EBITA (OM) | 110 | 12 | 22 | 30 | 35 | 99 | 154 | 170 |

| EBITA margin | 6% | 3% | 5% | 6% | 7% | 5% | 7% | 7% |

| Earning | ||||||||

| EBITA | 345 | 67 | 80 | 88 | 103 | 338 | 447 | 489 |

| EBITA Margin (%) | 8.3% | 5.3% | 6.2% | 7.1% | 7.6% | 6.6% | 8.0% | 8.2% |

| EBIT | 328 | 61 | 73 | 82 | 96 | 312 | 424 | 468 |

| EBIT Margin (%) | 7.9% | 4.9% | 5.7% | 6.5% | 7.1% | 6.1% | 7.6% | 7.9% |

| Diluted EPS | 4.98 | 0.78 | 0.61 | 0.78 | 1.06 | 3.23 | 4.98 | 5.83 |

| Source: Hanza & Redeye Research |

Valuation

We lower our Base Case somewhat to SEK 73 (90) on the back of reduced forecasts and a softer outlook. Nevertheless, we keep our positive view and see substantial upside potential if the 2025 targets are reached.

| Fair Value Range - Assumptions | |||

| Bear Case | Base Case | Bull Case | |

| Value per share, SEK | 23 | 73 | 99 |

| Sales CAGR | |||

| 2024 - 2031 | 4% | 6% | 7% |

| 2031 - 2041 | 1% | 3% | 3% |

| Avg EBIT margin | |||

| 2024 - 2031 | 7% | 8% | 9% |

| 2031 - 2041 | 5% | 8% | 9% |

| Terminal EBIT Margin | 6% | 8% | 9% |

| Terminal growth | 2% | 2% | 2% |

| WACC | 10% | 10% | 10% |

| Source: Redeye Research |

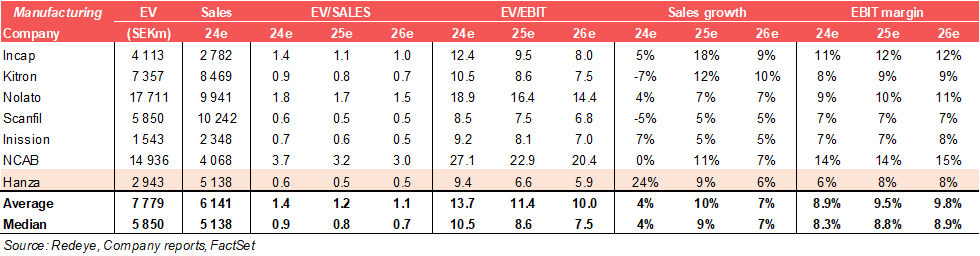

Peer Valuation

Despite the strong operational performance in recent years, with high growth and improving margins during 2023, Hanza is still trading at a discount (~20% on EV/EBIT) to the average, although often bigger, manufacturing service companies. We believe the discount will decrease further, given that Hanza continues its strong operational performance.

Investment thesis

Case

Riding the Back-Shoring Trend with its Unique Cluster Strategy

Evidence

Proven Track-Record in Mature Clusters

Challenge

Cyclical Exposure Through Customers’ Volume Fluctuations

Challenge

Lack of transferability

Valuation

Fair Value SEK 73

Quality Rating

People: 4

Hanza receives a high rating for people, as both management and owners have favorable characteristics. CEO Erik Stenfors has vast experience of the manufacturing service industry, including being the founder and CEO of both Note and Hanza. Hanza's largest sharholder is Gerald Engström, the founder and majority owner of Systemair. As a result, Hanza also has the support of a product company veteran.

Business: 3

Lacking clear differentiators, competition in the manufacturing service industry is typically tough. While Hanza has a unique take on the industry, we believe it is still difficult for it to increase prices for example. All the same, Hanza is a close and important partner for several of its customers. Moreover, it has decent diversification across both sectors and customers. Overall, Hanza receives an average rating for Business.

Financials: 3

While Hanza's near-term financial performance is strong, the long-term track-record has been weak, which lowers the Financials rating. Its solid financial position is positive, while the low-margin nature of its business is negative for the rating. In summary, Hanza receives an average rating for Financials. Several consecutive years of solid performance would lift the rating, though.

Financials

| Income statement | |||||

| SEKm | 2023 | 2024e | 2025e | 2026e | 2027e |

| Revenues | 4,154.0 | 5,158.2 | 5,611.9 | 5,947.9 | 6,304.1 |

| Cost of Revenue | 2,334.0 | 3,120.7 | 3,472.0 | 3,680.3 | 3,901.1 |

| Operating Expenses | 1,345.3 | 1,532.5 | 1,522.6 | 1,600.1 | 1,678.0 |

| EBITDA | 464.7 | 485.0 | 605.4 | 655.6 | 713.0 |

| Depreciation | 65.6 | 77.0 | 87.4 | 96.1 | 111.3 |

| Amortizations | 17.0 | 26.4 | 23.0 | 20.4 | 16.6 |

| EBIT | 328.0 | 311.7 | 424.1 | 468.2 | 514.3 |

| Shares in Associates | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Interest Expenses | -80.0 | -149.5 | -164.7 | -164.7 | -164.7 |

| Net Financial Items | 80.0 | 149.5 | 164.7 | 164.7 | 164.7 |

| EBT | 248.0 | 162.2 | 259.4 | 303.5 | 349.6 |

| Income Tax Expenses | -33.0 | -22.6 | -44.1 | -51.6 | -59.4 |

| Net Income | 215.0 | 139.6 | 215.3 | 251.9 | 290.2 |

| Balance sheet | |||||

| Assets | |||||

| Non-current assets | |||||

| SEKm | 2023 | 2024e | 2025e | 2026e | 2027e |

| Property, Plant and Equipment (Net) | 714.0 | 893.1 | 1,045.0 | 1,210.0 | 1,375.5 |

| Goodwill | 387.0 | 529.0 | 529.0 | 529.0 | 529.0 |

| Intangible Assets | 77.0 | 131.6 | 108.5 | 88.1 | 71.5 |

| Right-of-Use Assets | 186.0 | 230.0 | 230.0 | 230.0 | 230.0 |

| Other Non-Current Assets | 23.0 | 33.0 | 33.0 | 33.0 | 33.0 |

| Total Non-Current Assets | 1,387.0 | 1,816.7 | 1,945.5 | 2,090.1 | 2,239.1 |

| Current assets | |||||

| SEKm | 2023 | 2024e | 2025e | 2026e | 2027e |

| Inventories | 936.0 | 1,233.9 | 1,232.0 | 1,305.9 | 1,384.3 |

| Accounts Receivable | 175.0 | 257.1 | 252.0 | 267.1 | 283.1 |

| Other Current Assets | 91.0 | 154.2 | 168.0 | 178.1 | 188.8 |

| Cash Equivalents | 340.0 | 496.0 | 640.3 | 667.6 | 718.0 |

| Total Current Assets | 1,542.0 | 2,141.1 | 2,292.3 | 2,418.7 | 2,574.2 |

| Total Assets | 2,929.0 | 3,957.8 | 4,237.8 | 4,508.8 | 4,813.3 |

| Equity and Liabilities | |||||

| Equity | |||||

| SEKm | 2023 | 2024e | 2025e | 2026e | 2027e |

| Non Controlling Interest | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Shareholder's Equity | 1,345.0 | 1,527.2 | 1,707.6 | 1,905.7 | 2,132.9 |

| Non-current liabilities | |||||

| SEKm | 2023 | 2024e | 2025e | 2026e | 2027e |

| Long Term Debt | 326.0 | 509.0 | 509.0 | 509.0 | 509.0 |

| Long Term Lease Liabilities | 114.0 | 147.0 | 147.0 | 147.0 | 147.0 |

| Other Non-Current Lease Liabilities | 159.0 | 198.0 | 198.0 | 198.0 | 198.0 |

| Total Non-Current Liabilities | 599.0 | 854.0 | 854.0 | 854.0 | 854.0 |

| Current liabilities | |||||

| SEKm | 2023 | 2024e | 2025e | 2026e | 2027e |

| Short Term Debt | 196.0 | 406.0 | 406.0 | 406.0 | 406.0 |

| Short Term Lease Liabilities | 53.0 | 55.0 | 55.0 | 55.0 | 55.0 |

| Accounts Payable | 450.0 | 668.4 | 728.0 | 771.7 | 818.0 |

| Other Current Liabilities | 286.0 | 447.3 | 487.2 | 516.4 | 547.4 |

| Total Current Liabilities | 985.0 | 1,576.6 | 1,676.2 | 1,749.1 | 1,826.4 |

| Total Liabilities and Equity | 2,929.0 | 3,957.8 | 4,237.8 | 4,508.8 | 4,813.3 |

| Cash flow | |||||

| SEKm | 2023 | 2024e | 2025e | 2026e | 2027e |

| Operating Cash Flow | 277.0 | 594.4 | 489.3 | 413.1 | 461.1 |

| Investing Cash Flow | -296.0 | -573.9 | -239.2 | -261.2 | -276.9 |

| Financing Cash Flow | 217.0 | 126.5 | -105.7 | -124.7 | -133.8 |

Rating definitions

The team

Disclosures and disclaimers

Contents

Review of Q1 2024

Softer Than Expected

Main Markets

Other Markets

Large Inventory in Orbit One

Estimate Revisions: Reduced Forecasts for 2024 and 2025

Valuation

Investment thesis

Quality Rating

Financials

Rating definitions

The team

Download article