Arise Q2 2024 Preview: Weaker-than-expected spot prices but favourable price hedges

Research Update

2024-07-12

07:00

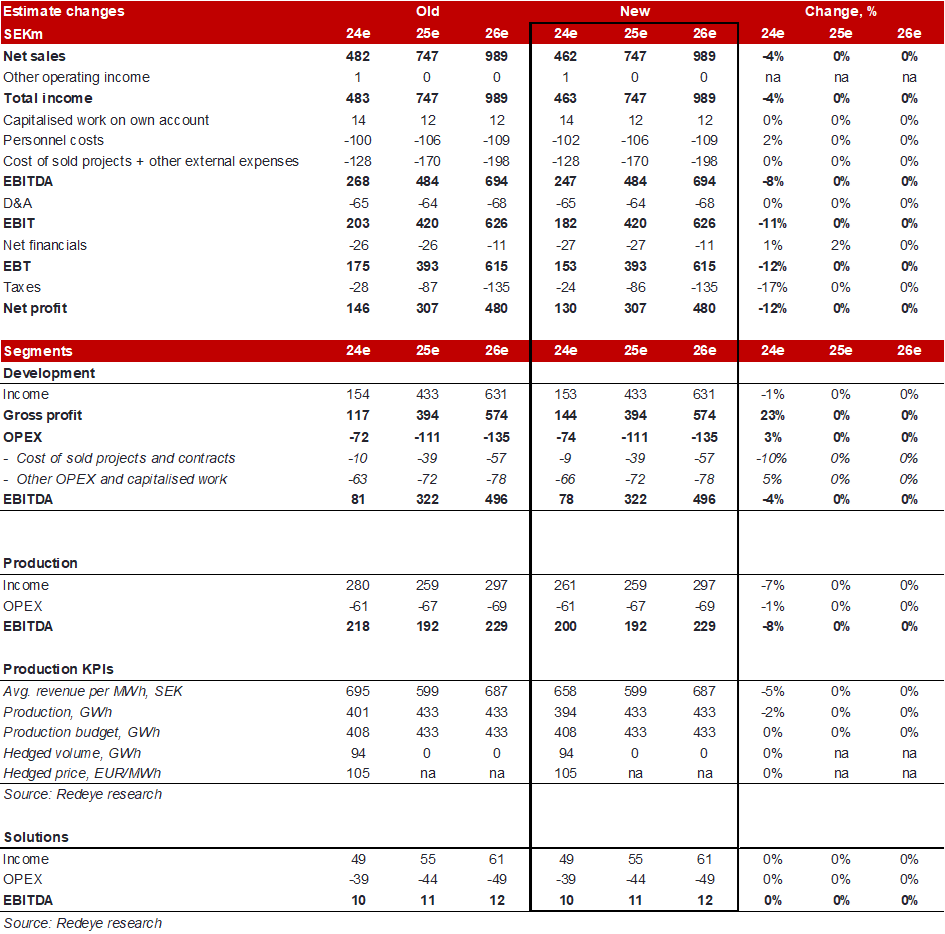

Redeye updates its estimates ahead of Arise’s Q2 report, which is due on 17 July. The quarter showed lower market prices for electricity than expected, which has a negative effect on our Q2 estimates. However, Arise has hedged around 25% of our expected Q2 production at favourable prices, which mutes this negative effect. Furthermore, we expect a significant production contribution from the new wind farm Lebo, as well as revenues from ongoing constructions plus the earn-out payment from the finalised project Ranasjö- and Salsjöhöjden in the development segment. The estimate changes do not affect our fair value range or base case.

Mattias Ehrenborg

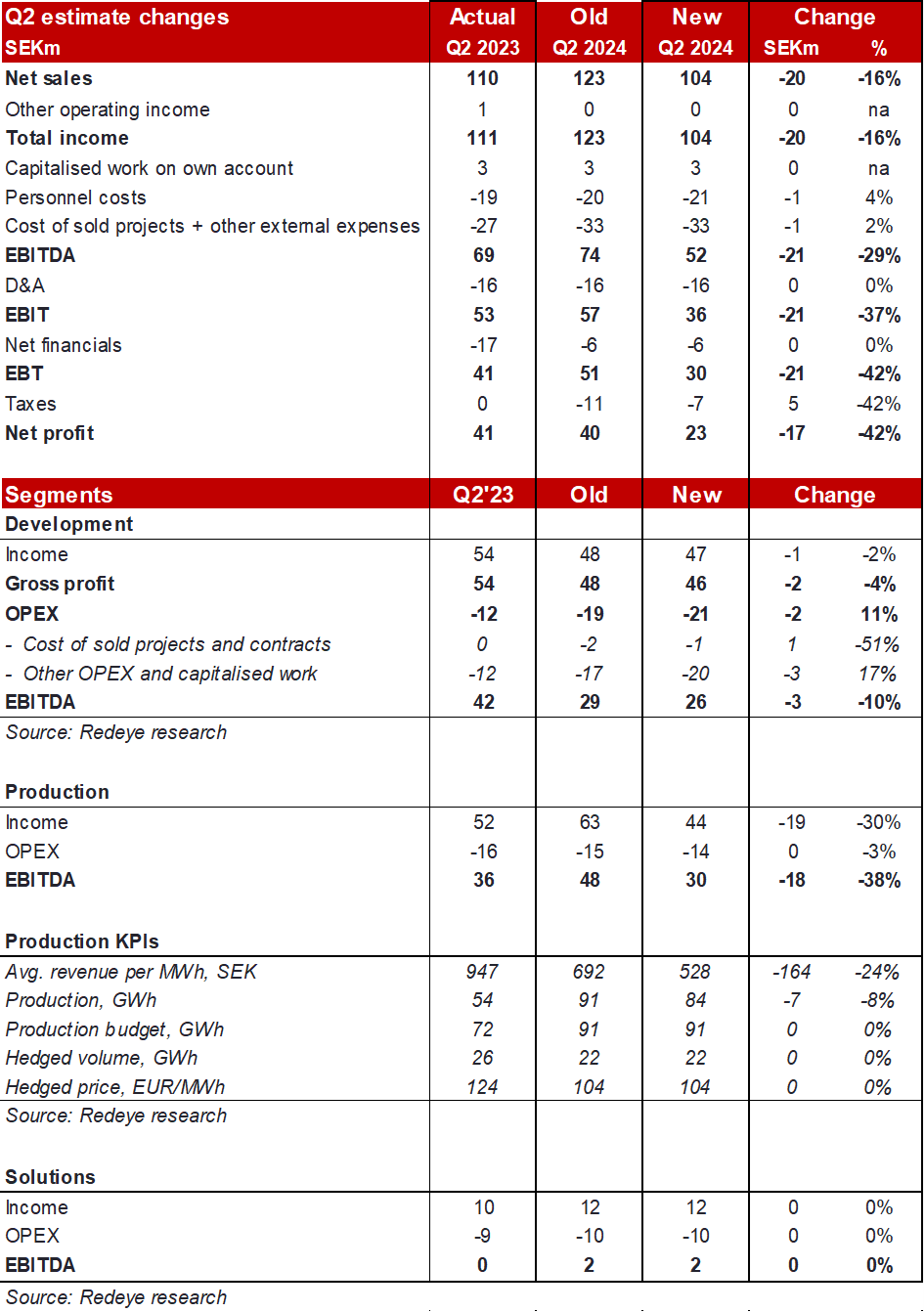

Updated production numbers

The Q2 2024 winds seem to have been significantly stronger than in Q2 2023 -which, according to our calculations, should generate 68.5GWh in Q2’24 vs 53.9GWh in Q2’23. This compares to the budget of 72.1GWh (also our previous est.). In addition to these numbers, we also expect Lebo (fully operational since May) to contribute with 15GWh in the quarter - bringing the total Q2 production to 83.5GWh (prev. est: 91.0GWh).

Lower-than-expected spot prices

Q2 2024 presented lower-than-expected spot prices in both SE3 and SE4. We previously expected a Q2 SE3 price of EUR45/MWh vs the actual EUR31/MWh. For SE4, we expected a price of EUR60/MWh vs the actual EUR51/MWh. We also expected a capture price discount of 15% - which, according to our calculations, seems to amount to 30% in Q2, negatively impacting our estimates. All in all, our expected realised revenue/MWh is reduced from SEK692/MWh to SEK528/MWh – partly saved by successful price hedges (25% of prod.) made at EUR104/MWh. Without the hedges, we believe Arise would realise a revenue of SEK321/MWh.

Development numbers are driven by ongoing constructions and earn-outs

We expect ongoing constructions to generate SEK19m in revenue recognition and the EUR6.6m earn-out payment for Rana- and Salsjöhöjden to add EUR2.4m to the P&L. We also expect a minor negative FX effect of SEK3m to affect Q2 numbers due to the revaluation of receivables related to ongoing constructions. A reversed effect of SEK9m took place in Q1 2024. Overall, we expect Arise to report a total EBITDA of SEK52m (SEK69m in Q2’23), vs our previous estimate of SEK74m.

Key financials

| SEKm | 2022 | 2023 | 2024e | 2025e | 2026e |

| Total Revenue | 1,169.0 | 507.0 | 463.1 | 747.4 | 989.4 |

| Revenue Growth | 243% | -56.6% | -8.7% | 61.4% | 32.4% |

| EBITDA | 851.0 | 286.0 | 247.1 | 483.9 | 693.8 |

| EBIT | 790.0 | 222.0 | 181.6 | 419.6 | 626.2 |

| EBIT Margin | 67.6% | 43.8% | 39.2% | 56.1% | 63.3% |

| Net Income | 772.0 | 205.0 | 129.5 | 306.5 | 479.9 |

| EV/EBITDA | 2.5 | 7.7 | 10.3 | 4.5 | 2.5 |

| EV/EBIT | 2.6 | 9.9 | 14.1 | 5.1 | 2.7 |

Disclosures and disclaimers