Vertiseit Q2: Sales and ARR as Expected, Stronger Profit

Research Note

2024-07-18

06:40

Redeye strengthens its positive view of Vertiseit following a Q2 report that exceeds our expectations. Organic ARR growth was strong at 21%, and the margins continue to improve. We will likely increase our forecasts and Base Case somewhat.

JB

Fredrik Nilsson

Jacob Benon

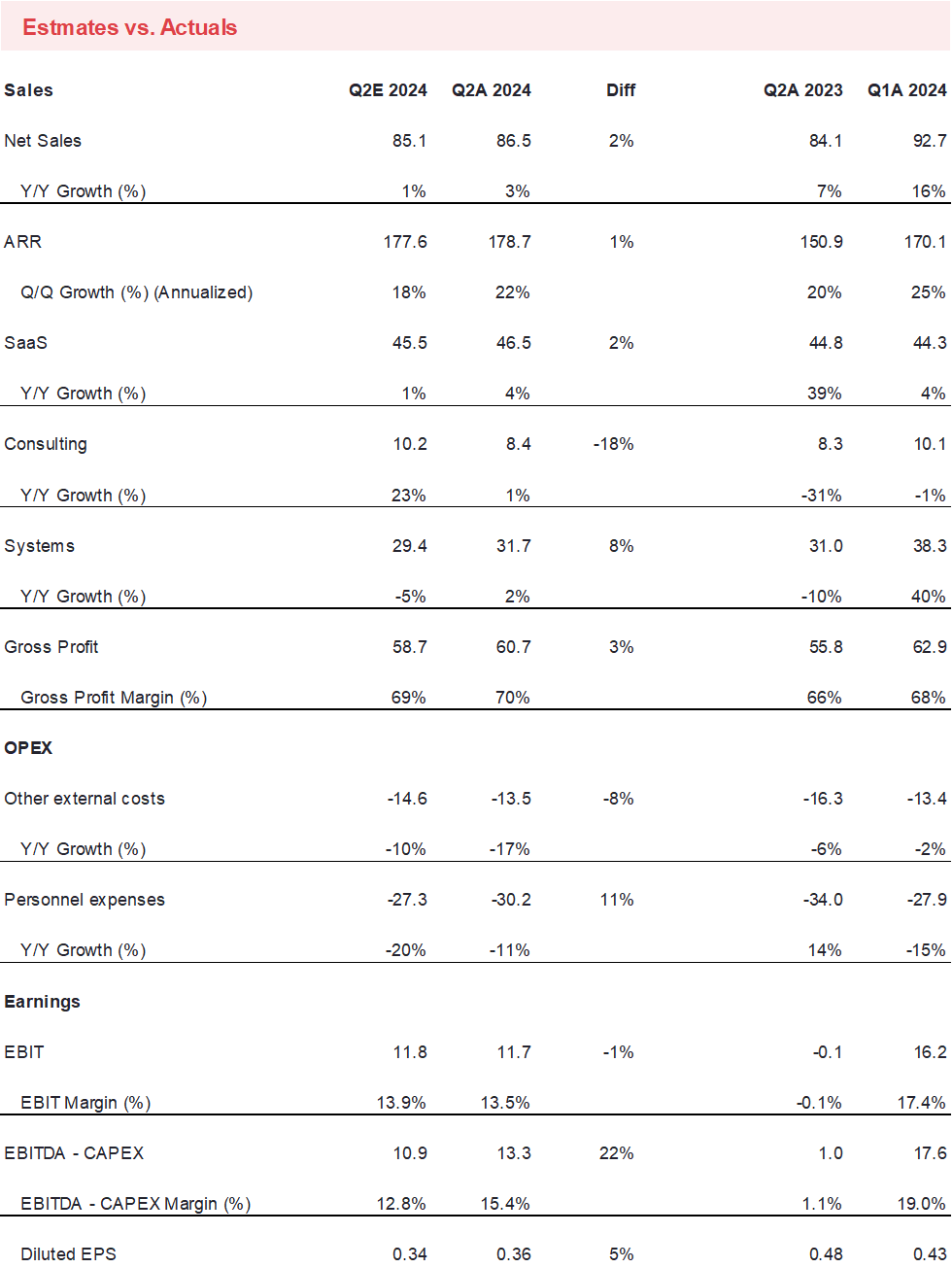

- ARR increased organically by 21% y/y, and the annualized q/q organic growth was 21% as well. The ARR was 1% above our expectations. Overall, a solid quarter in terms of ARR, which is the most important metric.

- Sales increased by 3% y/y (negatively affected by the divestment of MultiQ Denmark) and beat our forecast by 2%. Consulting was lower, while both SaaS and Systems exceeded our expectations.

- The gross profit beat our expectations by 3%, following slightly stronger sales than expected, and the gross margin roughly matched our forecast.

- EBITDA – CAPEX (Cash EBITDA) – our definition includes capex in tangible fixed assets, unlike Vertiseit; we might change our definition to align – was SEK13.3m (1.0), corresponding to an EBITDA – CAPEX margin of 15.4% (1.1). Our forecast was SEK10.9m, and the deviation was due to a somewhat higher gross profit and slightly lower D&A.

- The SaaS metrics continue to improve, with an R12m churn of 4.4% and an NRR of 113%. Both are solid numbers, placing Vertiseit among the top 25% in the listed Nordic SaaS space (compared to Q1 figures, as very few have published Q2 reports yet).

- Free cash flow was solid at SEK13.3m, partly thanks to a positive contribution from NWC.

- Overall, it is a solid report, with most lines coming in somewhat above our expectations. We will likely increase our forecasts and Base Case somewhat.

Disclosures and disclaimers