Arise: A solid and undramatic quarter

Research Update

2024-07-18

11:00

Redeye makes minor estimate revisions following Arise’s Q2 report, which was very much in line with Redeye’s estimates. We think the quarter was stable, and although the spot prices were low, Arise realised a high revenue per MWh due to favourable price hedges. Ongoing constructions are proceeding according to plan, and the project portfolio is growing and maturing – which we think supports Arise’s journey to reaching its financial targets.

Mattias Ehrenborg

Contents

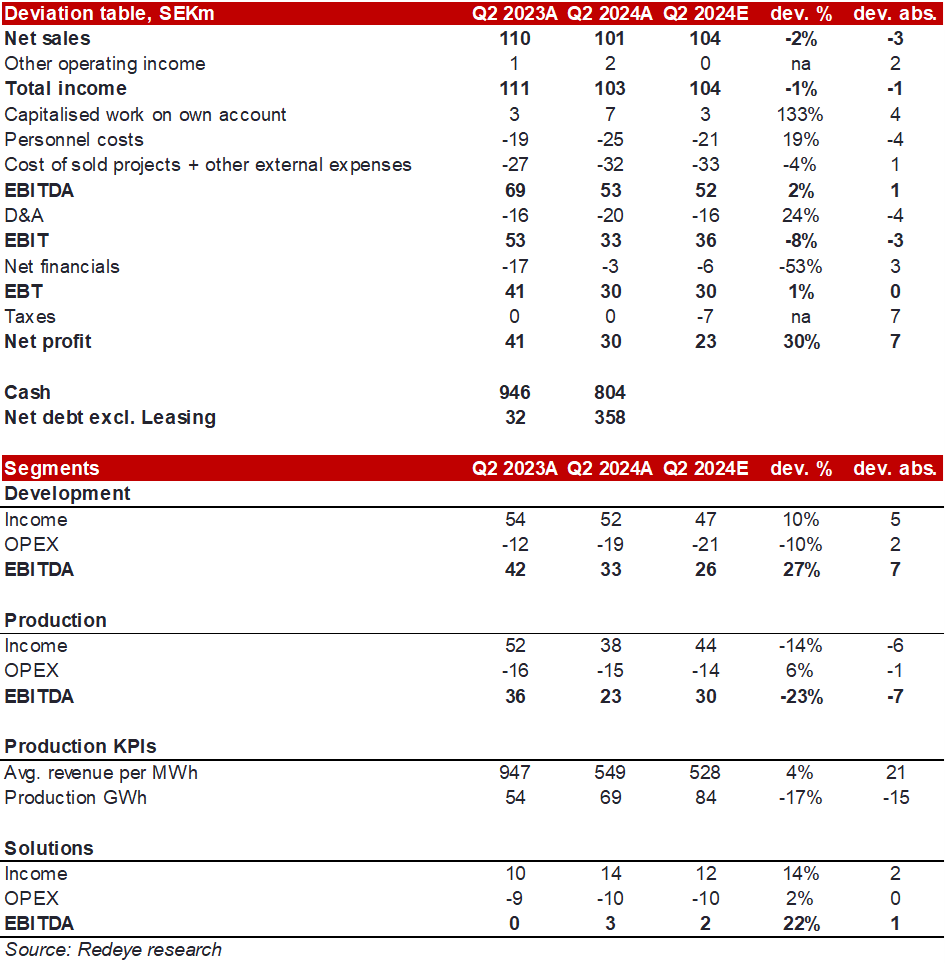

A quarter in line with our estimates

Arise reported Q2 2024 sales of SEK101m (SEK110m in Q2 2023), relative to our estimate of SEK104m. Q2 2024 EBITDA amounted to SEK53m (SEK69m in Q2 2023) relative to our estimate of SEK52m. The deviation from last year’s numbers is primarily explained by lower revenue recognition from projects in this quarter. None of the segments presented any surprises, where the ongoing constructions proceeded according to plan, and the production segment realised a revenue per MWh (SEK549/MWh) in line with our estimates.

Minor estimate revisions but increased confidence

We make very minor estimate revisions on the back of Arise’s Q2 report. Our key takeaways from the report are the following: Arise keeps growing its project portfolio and advances projects into the late-stage portfolio, Arise still targets to make a transaction in 2024, Lebo has been fully operational since May, and investor appetite seems to be increasing following lower interest rates and more stable CAPEX levels. In our view, the report was undramatic but increases our confidence in the investment case of Arise and its progression towards reaching its financial targets.

The fair value range remains intact

Our fair value range of SEK22-111 with a base case of SEK79 remains intact. Going forward, we consider the main catalyst to be a project divestment in H2 2024. With a Q2 cash balance of SEK804m, solid cash flow generation from production, and limited capital requirements going forward (apart from Pohjan Voima earnout), Arise has many opportunities to deploy this cash to create shareholder value.

Key financials

| SEKm | 2022 | 2023 | 2024e | 2025e | 2026e |

| Total Revenue | 1,169.0 | 507.0 | 463.5 | 750.4 | 993.9 |

| Revenue Growth | 243% | -56.6% | -8.6% | 61.9% | 32.4% |

| EBITDA | 851.0 | 286.0 | 246.1 | 483.5 | 694.5 |

| EBIT | 790.0 | 222.0 | 169.9 | 406.1 | 614.2 |

| EBIT Margin | 67.6% | 43.8% | 36.7% | 54.1% | 61.8% |

| Net Income | 772.0 | 205.0 | 128.9 | 294.5 | 470.5 |

| EV/Sales | 1.8 | 4.4 | 5.6 | 2.0 | 1.0 |

| EV/EBIT | 2.6 | 9.9 | 15.2 | 5.4 | 2.9 |

Disclosures and disclaimers

Contents