Vertiseit Q1 2023: Solid ARR Growth, Higher OPEX

Research Note

2023-04-27

15:48

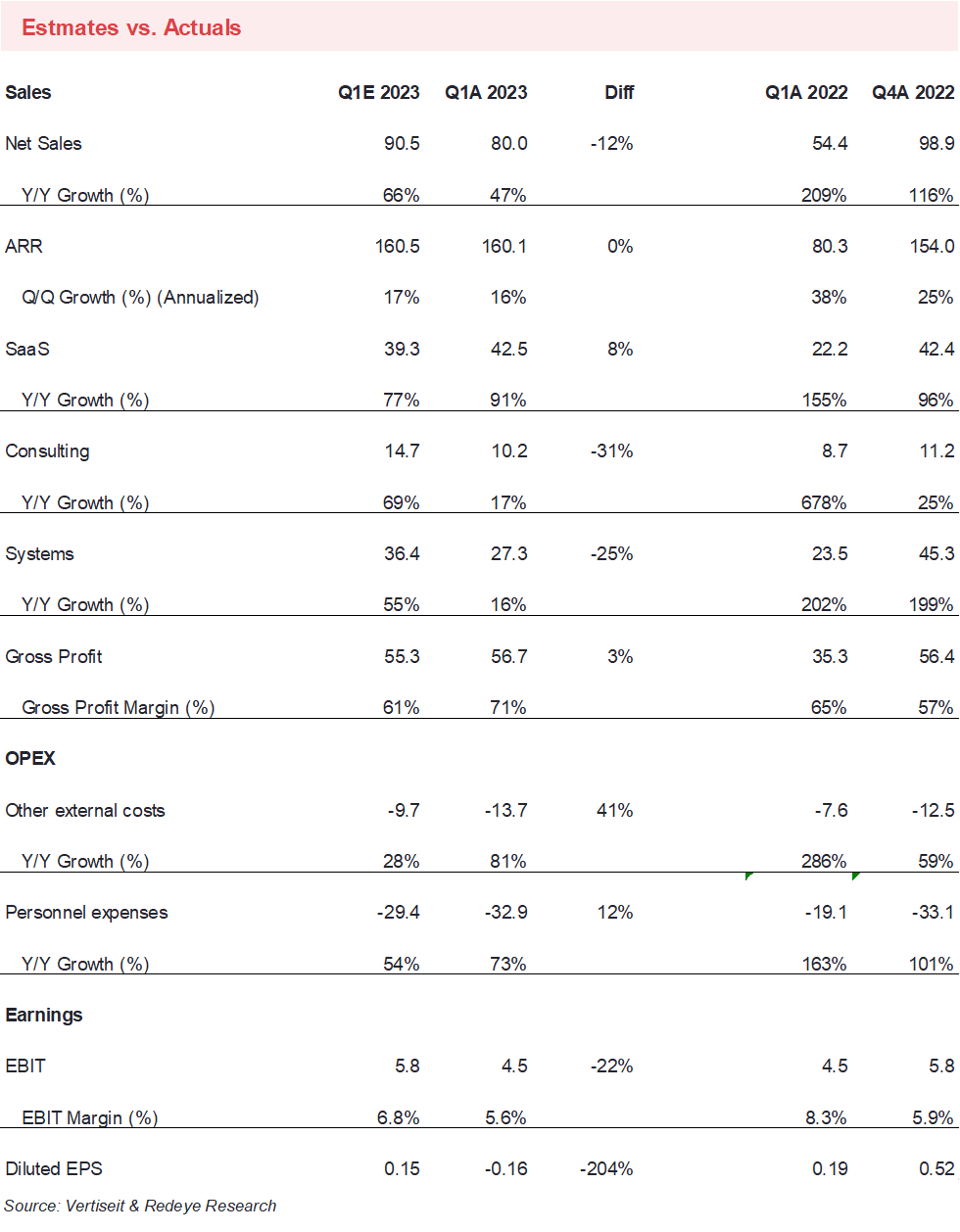

Redeye will likely leave its Base Case and forecasts roughly unchanged following Vertiseit’s Q1 report. The ARR continued to grow at a solid pace, matching our forecast. While gross profit beat our estimate slightly, higher OPEX resulted in a somewhat softer EBIT.

Fredrik Nilsson

- ARR grew by 21% organically y/y and the sequential growth was 4.6%. The ARR growth matched our forecasts, although we include the SEKc16m in ARR related to businesses Vertiseit wants to divest. Hence, the SEK16m difference to Vertiseit’s number.

- While sales came in 12% below expectations, mostly due to lower System sales, Gross profit largely matched our forecasts. As Vertiseit has different revenue streams with large variations in gross margins, we believe gross profit is more relevant than net sales.

- As usual, SaaS revenue beat our forecast somewhat while Consulting came in soft, likely due to some SaaS revenues not being included in the ARR.

- EBIT was SEK4.5m (4.5), somewhat below our forecast of SEK5.8m. The deviation was due to larger OPEX, both Other external costs and Personnel expenses. We might have underestimated the impact of finetuning the new group-common IT systems.

- Management sees a solid market, particularly in the automotive and grocery segments.

- For the first time, Vertiseit publishes a comprehensive table of SaaS metrics for the full group, which we appreciate. Previously, SaaS metrics was published only for Dise. Churn was c8% on annualized numbers while the NRR was 101%. As Grassfish typically targets larger customers than Dise, we did expect somewhat lower churn and higher NRR. On the other hand, the CAC/payback was impressive 6 months. We expected a higher number for Grassfish. However, we do not want to make any major statements about the SaaS metrics after only one quarter.

- We will likely leave our forecasts and Base Case largely unchanged.

Disclosures and disclaimers