Efecte: Strong Momentum in New Sales

Research Update

2023-08-14

06:45

Redeye retains its positive view of Efecte following the Q2 report. New sales was strong and compensated for a somewhat softer NRR, although still at a healthy level. Efecte sticks to its 2023 guidance, and we keep our forecasts roughly unchanged and retain our Base Case.

FN

MS

Fredrik Nilsson

Mark Siöstedt

Contents

Review of Q2 2023

MRR: Solid Growth Driven by Strong New Sales

Sales: Overall as Expected - Service Sales Seeing a Negative Impact from a Softer Market

OPEX: Lower Than Expected

Profit and Cash Flow: Slightly Stronger Adjusted EBITDA

Other Highlights from the Report

Estimate Revisions: Minor Revisions

Valuation

Investment thesis

Quality Rating

Financials

Rating definitions

The team

Download article

Continued Momentum in New Sales

MRR was EUR1377k (1097k), corresponding to a y/y growth of 26%, and matched our forecast. New sales was solid at 16% y/y, beating our forecast of 13%, while the NRR of 109% came in somewhat short of our estimate of 112.5%. Adjusted EBITDA was EUR0.1m (0.1), corresponding to an adjusted EBITDA margin of 1.1% (2.5). Our forecast was EUR-0.2m and -3.7%, and the beat was mainly due to lower OPEX. FCF for H1 2023 was positive due to net working capital contributing positively, thanks to Efecte’s business model.

Further Traction Among Swedish Municipalities

The focus on the public sector, partly done to offset the expected decline in demand from private customers in the softening market, has turned out well so far. After winning a tender with Helsingborg in Q1, Efecte followed up with Uppsala this quarter. Thus, Efecte seems to gain traction among larger Swedish municipalities (Uppsala and Helsingborg rank fourth and eighth in population). In total, Efecte won 35 new customers during H1 2023 compared to 21 in H1 2022. However, new customers from partners declined to four compared to ten last year.

Base Case Unchanged at EUR15

We leave our Base Case unchanged at EUR15. So far, we argue Efecte has handled the softer market conditions very well, highlighted by solid growth from New sales and an NRR remaining in healthy territory. We believe Efecte is a low-risk, financed (net cash remains positive despite the acquisition of InteliWISE), and attractively valued growth story. Q2 2023 marks the 23 consecutive quarter with SaaS revenue growth above 20%. We believe improving margins over the coming years will trigger a higher multiple valuation of Efecte in terms of EV/S.

Key financials

| SEKm | 2022 | 2023e | 2024e | 2025e | 2026e |

| Revenues | 21.6 | 25.0 | 29.2 | 34.2 | 39.8 |

| Revenue Growth | 21.7% | 15.5% | 17.1% | 17.1% | 16.3% |

| EBIT | -0.86 | -1.2 | 0.65 | 2.4 | 4.2 |

| EBIT Margin | -4.0% | -5.0% | 2.2% | 6.9% | 10.5% |

| EV/Revenue | 2.9 | 2.3 | 1.9 | 1.6 | 1.3 |

| EV/EBIT | -73.6 | -46.4 | 86.2 | 22.8 | 11.9 |

| ARR | 15 | 18 | 22 | 27 | 32 |

| ARR Growth | 28.0% | 20.0% | 22.5% | 20.5% | 19.5% |

| EBITDA - CAPEX | -1.4 | -1.6 | 0.3 | 1.9 | 3.7 |

| EBITDA - CAPEX Margin | -6.4% | -6.3% | 1.1% | 5.5% | 9.2% |

| EV/ARR | 4.2 | 3.1 | 2.5 | 2.0 | 1.5 |

| EV/EBITDA - CAPEX | neg | neg | 169.06 | 28.47 | 13.62 |

EURm and not SEKm as stated above.

Review of Q2 2023

| Estmates vs. Actuals | ||||||

| Sales | Q2E 2023 | Q2A 2023 | Diff | Q2A 2022 | Q1A 2023 | |

| Net Sales | 6.3 | 6.2 | -1% | 5.3 | 6.0 | |

| Y/Y Growth (%) | 18% | 17% | 19% | 20% | ||

| SaaS | 4.1 | 4.1 | 1% | 3.3 | 4.0 | |

| Growth y/y | 23% | 25% | 24% | 28% | ||

| MRR (EURk) | 1377 | 1377 | 0% | 1097 | 1343 | |

| Growth y/y | 26% | 26% | 22% | 27% | ||

| Churn (R12M) | 4.5% | 4.9% | 0.4% | 2.2% | 4.7% | |

| Uplift (R12M) | 17.0% | 14% | -3.4% | 16.6% | 17.2% | |

| New sales (R12M) | 13.0% | 16% | 3.0% | 7.2% | 15.0% | |

| NRR R12m | 112.5% | 109% | -3.5% | 114.4% | 112.4% | |

| Services | 2.0 | 1.9 | -5% | 1.8 | 1.8 | |

| Y/Y Growth (%) | 10% | 5% | 15% | 9% | ||

| Earnings | ||||||

| Adjusted EBITDA | -0.2 | 0.1 | nmf | 0.1 | -0.2 | |

| Adjusted EBITDA margin | -3.7% | 1.1% | 2.5% | -2.6% | ||

| EBIT | -0.6 | -0.3 | nmf | -0.2 | -0.6 | |

| EBIT Margin (%) | -8.9% | -4.8% | -3.6% | -9.7% | ||

| Diluted EPS | -0.09 | -0.04 | nmf | 0.07 | -0.10 |

MRR: Solid Growth Driven by Strong New Sales

MRR was EUR1377k (1097k), up from EUR1343k in the last quarter, corresponding to a y/y growth of 26%. The outcome matched our forecast. New sales was solid at 16% y/y, beating our forecast of 13%, while the NRR of 109% came in somewhat short of our estimate of 112.5%. Churn was 4.9%, somewhat above our forecast of 4.5% and in line with management’s statement of a normalized churn during 2023 (2022 had a very low level of ~2%). Upsell to current customers was 14%, slightly lower than the 17% we expected. The upsell was likely affected by a higher share of customers being cautious about adding additional employees due to a more challenging economic environment. However, the difference is minor compared to recent quarters’ 16-17%.

Also, management points out that while lower and sometimes negative net recruitment among customers hurts upsell, upsell from customers adding new functionality tends to perform well during economic downturns. A likely reason is that customers are looking deeper into platforms they already have to improve efficiency at a limited cost. Considering the flexibility of the Efecte platform, the company saw many customers adding new functionality during the Covid-19 pandemic, and we believe a similar scenario is likely in the current conditions. However, the net effect of the softer market on upselling might be somewhat negative, nevertheless.

Considering the softening market, we find the New sales of 16% impressive. According to management, the Swedish public sector continued to do well, including a deal with Uppsala Municipality. Also, Spain signed another customer, and Finland had a solid quarter. Combined with the deal with Helsingborg municipality in Q1 2023, Efecte seems to gain traction among larger Swedish municipalities (Uppsala and Helsingborg rank fourth and eighth in population). In the Finnish market, smaller municipalities also use the Efecte platform, although usually through partners regarding the smallest ones. Thus, we believe the Swedish municipality market is an exciting opportunity for Efecte.

Although Efecte’s in-house customer generation held up well, the contribution from partners was impacted by a softer market - the difference relative to H1 2022 is rather substantial. During H1 2023, Efecte added 35 new customers, of which four came from partners, compared to 21 new customers, of which ten from partners, in H1 2022. While management points out that the numbers regard a small timeframe, it believes one explanation might be that the current market environment, with cautious customers, favours the in-house team over partners. A possible reason is that customers might believe it is “safer” to go with the software provider rather than a partner, especially new partners. While we get the impression that management is satisfied with the quarter, for good reasons, considering the strong New sales in the softening market conditions, the customer intake from partners is an exception.

Source: Efecte

The MRR and its growth rate are important metrics to follow in Efecte. The MRR is a leading indicator of SaaS revenue growth. While Efecte has a substantial share of Service revenue, SaaS is the most important revenue type in Efecte, with ~80% gross margins.

Churn is the share of SaaS revenue lost from customers cancelling their subscriptions. While the churn levels vary substantially depending on vertical and customer size, due to bankruptcy rates, lower churn is better and typically indicates satisfied customers. Generally, for a company targeting larger B2B customers, like Efecte, we believe 5% or below is a healthy level. While the churn likely includes some unsatisfied customers, we believe most of Efecte’s churn is caused by M&A and bankruptcies.

Uplift or upsell is the growth from current customers, i.e., those who were also customers last year. In general, a high uplift indicates satisfied customers (unsatisfied customers are unlikely to expand). However, uplifts vary depending on customer segment and the packaging of the software, land and expand strategies targeting enterprise customers should have higher uplift, for example. Efecte mainly gains its uplift from additional seats (customers growing) and expansion of scope (customers adding more solutions such as IGA or ESM to ITSM).

New sales is the growth from new customers who have become customers of Efecte during the last 12 months.

Sales: Overall as Expected - Service Sales Seeing a Negative Impact from a Softer Market

Total sales largely matched our forecast of EUR6.3 and amounted to EUR6.2m (5.3), corresponding to 17% growth y/y. SaaS revenue matched our expectations, while Service revenue was somewhat softer. According to management, the softer market conditions have negatively impacted Service revenue, although the demand for Efecte’s professional service remains healthy. Maintenance related to Licenses continued to decline, and License revenue was zero, highlighting that Efecte is now a 100% SaaS business with in-house professional services.

Source: Efecte

OPEX: Lower Than Expected

Overall, OPEX came below our forecast of EUR-5.6m and was EUR-5.3m (-4.7). The number of employees was higher than anticipated, while the cost per employee was lower than we expected. Efecte does not split personnel expenses and other external costs in its Business Reviews (Q1 and Q3), so we calculate all OPEX per employee. According to management, an increased focus on costs has, for example, resulted in fewer sub-consultants and more employees. The numbers support that statement.

Efecte spent EUR2.4m (2.3) on R&D during the first half of 2023, corresponding to 20% (22) of net sales. About 30% was capitalized, which we believe is a reasonable level.

Profit and Cash Flow: Slightly Stronger Adjusted EBITDA

Adjusted EBITDA was EUR0.1m (0.1), corresponding to an adjusted EBITDA margin of 1.1% (2.5). Our forecast was EUR-0.2m and -3.7%, and the beat was mainly due to lower OPEX. Free cash flow (for H1 2023, all other numbers consern Q2 2023) was EUR0.5m (0.7). Efecte’s FCF, like in H1 2023, typically has a positive contribution from net working capital due to Efecte’s business model.

By the end of the quarter, Efecte’s net debt was EUR-1.8m.

Other Highlights from the Report

Product

In addition to the product highlights listed above, the ITSM Essential package went “ready for sale” during the quarter. The package aims to provide new customers with a simpler and less expensive method to begin their service management journey while retaining the Efecte platform’s flexibility to grow and expand. In addition to being a fast gateway onto the Efecte platform, we believe it also could be an interesting choice for smaller customers.

Retained Guidance

Efecte retains its guidance of SaaS net sales growth above 20% and positive adjusted EBITDA for 2023. As stated earlier, the SaaS sales growth rate is expected to decline in H2 2023 as InteliWISE numbers become part of the comparison period and due to an expected slight decrease in the organic growth rate.

We did not expect any changes to the guidance, and our forecasts largely align with the company’s guidance.

Digitalize and Automate 2023 – 19 September

This year’s main event will occur in Helsinki and online on 19 September from 09:00-14:25 CEST. The line-up includes, among others, Dr. Daniel Susskind, a Research Professor in Economics at King’s College London and a Senior Research Associate at the Institute for Ethics in Artificial Intelligence at Oxford University. His work explores the impact of technology, particularly AI, on work and society, and he is the author of the critically acclaimed and bestselling books The Future of the Professions and A World Without Work.

We believe the event is an excellent opportunity for investors to gain deeper insight into Efecte and its market.

For more information, see the event page.

Estimate Revisions: Minor Revisions

We leave our estimates roughly unchanged regarding both sales and profit. On a detailed basis, we make the following minor changes:

- Lowering our Uplift forecasts – Considering the current market conditions, we believe it is reasonable to expect a slightly lower upsell from current customers.

- Increasing our New sales forecasts – Although New sales should suffer from softer market conditions, Efecte seems to handle the situation well so far. Despite increasing our assumptions somewhat, we still expect a decline from the current levels.

- Lower our OPEX forecasts – Considering the outcome in this quarter, Efecte seems to handle cost control somewhat better than we expected.

Our 2023 forecasts assume a 0.4% EBITDA margin and 21.3% SaaS revenue growth, in line with management’s guidance.

Relative to Efecte’s long-term targets of EUR35m in sales and a double-digit EBITDA margin in 2025, we forecast EUR34.2m and 12.1%.

| Estimate Revisions | ||||||

| Sales | FYE 2023 | Old | Change | FYE 2024 | Old | Change |

| Net Sales | 25.0 | 25.1 | -1% | 29.2 | 29.7 | -1% |

| Y/Y Growth (%) | 15% | 16% | 17% | 18% | ||

| SaaS | 16.7 | 16.7 | 0% | 20.3 | 20.5 | -1% |

| Growth y/y | 21% | 22% | 22% | 23% | ||

| MRR (EURk) | 1524 | 1543 | -1% | 1867 | 1890 | -1% |

| Growth y/y | 20% | 22% | 23% | 23% | ||

| Churn (R12M) | 4.5% | 4.5% | 0% | 3.5% | 3.5% | 0% |

| Uplift (R12M) | 14.5% | 17.0% | -3% | 16.0% | 17.0% | -3% |

| New sales (R12M) | 10.0% | 9.0% | 1% | 10.0% | 9.0% | 1% |

| NRR R12m | 110.0% | 112.5% | -2% | 112.5% | 113.5% | -2% |

| Services | 7.4 | 7.5 | -2% | 8.1 | 8.3 | -3% |

| Y/Y Growth (%) | 7% | 9% | 9% | 10% | ||

| Earnings | ||||||

| EBITDA | 0.1 | -0.4 | -127% | 2.2 | 1.7 | 31% |

| EBITDA margin | 0.4% | -1.5% | 7.5% | 5.6% | ||

| EBIT | -1.2 | -1.7 | -29% | 0.7 | 0.1 | 552% |

| EBIT Margin (%) | -5.0% | -7.0% | 2.2% | 0.3% | ||

| Diluted EPS | -0.19 | -0.28 | -30% | 0.06 | -0.01 | -551% |

| Forecasts | ||||||||

| Sales | Q1A 2023 | Q2A 2023 | Q3E 2023 | Q4E 2023 | FYE 2023 | FYE 2024 | FYE 2025 | FYE 2026 |

| Net Sales | 6.0 | 6.2 | 6.0 | 6.7 | 25.0 | 29.2 | 34.2 | 39.8 |

| Y/Y Growth (%) | 20% | 17% | 13% | 13% | 15% | 17% | 17% | 16% |

| SaaS | 4.0 | 4.1 | 4.2 | 4.4 | 16.7 | 20.3 | 24.7 | 29.6 |

| Growth y/y | 28% | 25% | 16% | 17% | 21% | 22% | 21% | 20% |

| MRR (EURk) | 1343 | 1377 | 1398 | 1524 | 1524 | 1867 | 2250 | 2688 |

| Growth y/y | 27% | 26% | 20% | 20% | 20% | 23% | 21% | 20% |

| Churn (R12M) | 4.7% | 4.9% | 4.5% | 4.5% | 4.5% | 3.5% | 3.5% | 3.5% |

| Uplift (R12M) | 17.2% | 14.3% | 14.5% | 14.5% | 14.5% | 16.0% | 15.0% | 15.0% |

| New sales (R12M) | 15.0% | 16.2% | 10.0% | 10.0% | 10.0% | 10.0% | 9.0% | 8.0% |

| NRR R12m | 112.4% | 109.4% | 110.0% | 110.0% | 110.0% | 112.5% | 111.5% | 111.5% |

| Services | 1.8 | 1.9 | 1.7 | 2.1 | 7.4 | 8.1 | 8.7 | 9.4 |

| Y/Y Growth (%) | 9% | 5% | 6% | 7% | 7% | 9% | 9% | 8% |

| Earnings | ||||||||

| EBITDA | -0.3 | 0.0 | 0.1 | 0.3 | 0.1 | 2.2 | 4.2 | 6.3 |

| EBITDA margin | -4.4% | 0.5% | 1.1% | 4.0% | 0.4% | 7.5% | 12.1% | 15.8% |

| EBIT | -0.6 | -0.3 | -0.3 | -0.1 | -1.2 | 0.7 | 2.4 | 4.2 |

| EBIT Margin (%) | -9.7% | -4.8% | -4.6% | -1.1% | -5.0% | 2.2% | 6.9% | 10.5% |

| Diluted EPS | 0.00 | 0.00 | -0.05 | -0.02 | -0.19 | 0.06 | 0.26 | 0.48 |

Valuation

We leave our Base Case unchanged at EUR15. We believe Efecte is a low-risk, financed (net cash remains positive despite the acquisition of InteliWISE), and attractively valued growth story. Q2 2023 marks the 23 consecutive quarter with SaaS revenue growth above 20%. We believe improving margins over the coming years will trigger a higher multiple valuation of Efecte in terms of EV/S.

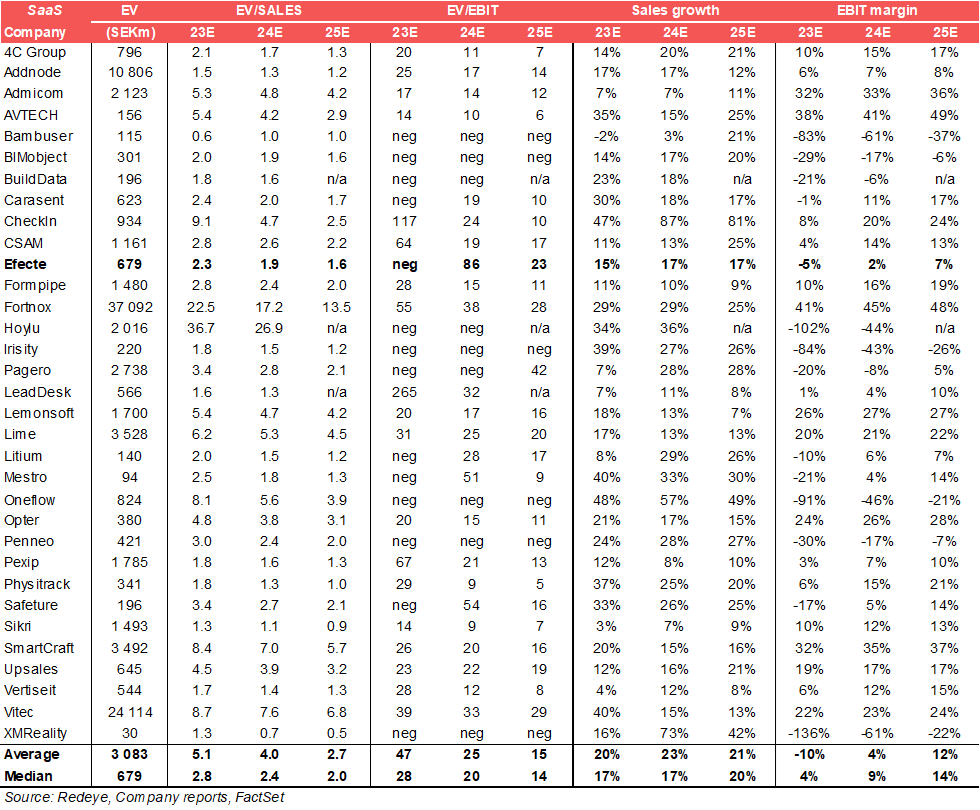

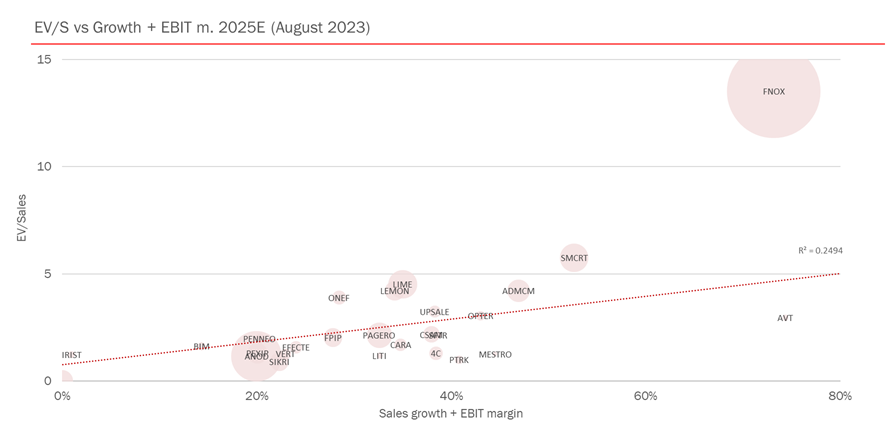

Peer Valuation

We believe the combination of a low EV/sales multiple (~2x 2024E), strong SaaS metrics, and a neutral cash flow make the risk/reward in Efecte attractive. The valuation risk is likely rather limited, and we see no risk for Efecte needing a share issue to fund its daily operations. So, we believe the key question is, can Efecte grow and reach solid profitability? Considering its solid SaaS metrics, we believe it can.

Investment thesis

Case

While running at zero margins favoring growth, Efecte is set to become highly profitable.

Evidence

A solid track record supports our view.

Challenge

Fighting the giants and local champions.

Challenge

Mediocre new sales limiting overall SaaS growth.

Valuation

Low EV/S does not consider future margin expansion.

Quality Rating

People: 4

Efecte receives an average rating for People for several reasons. First, we believe management has a balanced and honest, almost defensive approach to communication with analysts and investors. Second, our impression is that management has a deep understanding of the market and is upright with potential risks. Third, the reporting has high transparency with lots of SaaS metrics. All in all, we believe these traits reduce the risk of unpleasant surprises to investors. To gain a higher rating, the board and management must increase their shareholdings.

Business: 4

Efecte receives a high rating for Business for several reasons. First, Efecte has its proprietary software and has established a partner network to drive sales. Second, low churn and high net revenue retention suggest that customers are satisfied and high switching costs. Third, the business has a high share of recurring revenues and limited exposure to economic cycles. To receive a higher rating, Efecte must further strengthen its position on the European market.

Financials: 3

Efecte receives an average rating for Financials. Efecte's has a solid track record of high and stable sales growth, which increased the rating. While we believe Efecte will become highly profitable going forward, the Financials rating is mainly backward-looking, punishing Efecte for its low and negative profitability history. We expect Efecte's Financials rating to improve in the coming years, as we expect its profitability to improve.

Financials

EURm and not SEKm as stated above.

Rating definitions

The team

Disclosures and disclaimers

Contents

Review of Q2 2023

MRR: Solid Growth Driven by Strong New Sales

Sales: Overall as Expected - Service Sales Seeing a Negative Impact from a Softer Market

OPEX: Lower Than Expected

Profit and Cash Flow: Slightly Stronger Adjusted EBITDA

Other Highlights from the Report

Estimate Revisions: Minor Revisions

Valuation

Investment thesis

Quality Rating

Financials

Rating definitions

The team

Download article