Hexatronic: Tough Market Set to Rebound Around H2 2024

Research Update

2023-10-31

06:45

Redeye retains its positive view of Hexatronic despite cutting its forecasts for 2024 mainly. While the Q3 outcome aligned with the Trading Update, our previous 2024 forecasts seems too optimistic considering the current market environment. Nevertheless, we believe the mid/long-term case is still on, and the valuation multiple has decreased significantly despite lowered forecasts. Although the timing is uncertain, we believe the market will rebound in H2 2024, as investments in FTTH remain important for underpenetrated countries.

FN

RJ

Fredrik Nilsson

Rasmus Jacobsson

Contents

Review of Q3 2023

Sales: Negative Organic Growth Following Softer Market

EBITA and Margins: EBITA Margin as Expected – In Line with Target Despite Negative Organic Growth

Cash Flow: NWC Relative to R12m Sales Remains High

Acquisitions: USNet and ATG Technology

Estimate Revisions: 13-21% Cuts on 2024e

Valuation

Investment thesis

Quality Rating

Financials

Rating definitions

The team

Download article

Q3 In Line with Trading Update Guidance

Total sales was 3% below our forecast of SEK1 980m and amounted to SEK1 917m (1 729), corresponding to 11% growth y/y. The organic growth y/y was -13%. The negative organic growth aligned with management’s guidance in the Trading Update published on 22 September. It was mainly due to higher financing costs and inventory buildup in some markets, predominantly the US and Germany. EBITA was SEK296m, corresponding to an EBITA margin of 15.4% (18.3). Our forecast was SEK305m and 15.4%, and the slight miss was due to softer sales. The slightly lower gross margin than expected was compensated for by solid cost control on OPEX. Thus, despite the negative organic growth, Hexatronic obtained an EBITA margin in line with its 15-17% target.

Gradual Rebound Expected from H2 2024

Management believes the BEAD and similar programs elsewhere along with reduced inventory levels will positively affect demand in H2 2024, which is in line with what we have heard from other players in the industry. At the same time, consider the outcome of Q3, we believe the UK and US FTTH businesses – although some delayed projects hurt US FTTH in the quarter – are doing rather well, while US conduit & pipe and German FTTH experienced softer demand. Although the timing is uncertain, we believe the market will rebound in H2 2024, as investments in FTTH remain important for underpenetrated countries.

New Base Case SEK67 (87)

We cut our sales and EBITA forecasts by 13% and 21% for 2024. The decrease is due to the softening market and us increasing the risk-free rate from 2.5% to 3% in our WACC. While the near-term outlook is uncertain, we have a positive long-term view of Hexatronic and its markets. We lowered our Base Case to SEK67 (87).

Key financials

| SEKm | 2022 | 2023e | 2024e | 2025e | 2026e |

| Revenues | 6,574.0 | 8,334.3 | 8,458.0 | 9,181.8 | 10,063.3 |

| Revenue Growth | 88.3% | 26.8% | 1.5% | 8.6% | 9.6% |

| EBITDA | 1,235.9 | 1,589.5 | 1,475.7 | 1,640.9 | 1,790.8 |

| EBIT | 1,027.6 | 1,260.7 | 1,113.8 | 1,282.8 | 1,447.7 |

| EBIT Margin | 15.6% | 15.1% | 13.2% | 14.0% | 14.4% |

| Net Income | 793.0 | 842.9 | 753.0 | 884.9 | 1,013.5 |

| EV/Revenue | 4.6 | 0.9 | 0.8 | 0.6 | 0.5 |

| EV/EBIT | 29.3 | 5.9 | 5.7 | 4.4 | 3.2 |

Review of Q3 2023

| Estmates vs. Actuals | ||||||

| Sales | Q3E 2023 | Q3A 2023 | Diff | Q3A 2022 | Q2A 2023 | |

| Net Sales | 1980 | 1917 | -3% | 1729 | 2258 | |

| Y/Y Growth (%) | 15% | 11% | 4% | 36% | ||

| Sweden | 178 | 165 | -7% | 193 | 176 | |

| Growth y/y (SWE) | -8% | -15% | 45% | -28% | ||

| Rest of Europe | 824 | 893 | 8% | 752 | 1099 | |

| Growth y/y (EU) | 10% | 19% | 83% | 47% | ||

| North America | 823 | 671 | -18% | 644 | 828 | |

| Growth y/y (NA) | 28% | 4% | 159% | 58% | ||

| Rest of the World | 156 | 188 | 21% | 140 | 156 | |

| Growth y/y (RotW) | 11% | 34% | 22% | 7% | ||

| Other operating income | 15 | 11 | 22 | |||

| Costs | ||||||

| Gross Profit | 871 | 812 | 761 | 995 | ||

| Gross Margin | 44.0% | 42.4% | 44.0% | 44.1% | ||

| OPEX | -525 | -484 | -419 | -558 | ||

| Growth y/y | 25% | 15% | 57% | 37% | ||

| Earnings | ||||||

| EBITA | 305 | 296 | -3% | 317 | 405 | |

| EBITA Margin (%) | 15.4% | 15.4% | 18.3% | 17.9% | ||

| Diluted EPS | 0.93 | 0.85 | -9% | 1.30 | 1.27 |

Sales: Negative Organic Growth Following Softer Market

Total sales was 3% below our forecast of SEK1 980m and amounted to SEK1 917m (1 729), corresponding to 11% growth y/y. The organic growth y/y was -13%. The negative organic growth aligned with management’s guidance in the Trading Update published on 22 September. It was mainly due to higher financing costs and inventory buildup in some markets, predominantly the US and Germany.

Management expects its relevant markets to remain at the level seen in Q3 for the next few quarters. However, as Hexatronic, at least until Q2 2023, performed much better than the market, if its performance would converge toward the market, we could see further declines. That could happen if Hexatronic loses market share, which we find unlikely, or if its customers postpone FTTH projects to the same extent as the market. While we believe that is a more likely scenario than Hexatronic losing market share, we expect its main FTTH customers to sustain its activities. Also, we believe Hexatronic has a competitive offering with its system solutions – especially in the US market, where it has a market share of a mere 1%. Thus, we believe it has the potential to increase its market share.

On a regional basis, North America and Sweden had lower sales than we expected. At the same time, the Rest of Europe and the Rest of the World (now rebranded as APAC) came in stronger than we anticipated.

North America was 18% lower than we expected. The total growth was 4% y/y, thanks to the acquisition of Rochester Cable and higher sales in Canada. On the other hand, the demand for conduit and pipe was lower and considering the increased capacity from the Clinton factory, we expected higher sales. While all production lines are operational, in line with guidance, it seems like the demand is not there currently. The work with the Utah factory continues, and production is expected in Q3 2024. We believe management continuing its investments in Utah, which will open the Western US for BDI, indicates it is confident in a solid mid/long-term market for conduit and pipe. In addition, some FTTH deliveries have been delayed in the quarter, which, all else equal, should result in a stronger North America over the next quarters. Management believes the BEAD program will positively affect demand gradually from H2 2024, which is in line with what we have heard from other players in the industry.

Europe grew by 19% y/y and beat our forecast by 8%, thanks to several acquisitions and strong growth in Finland's and Austria’s relatively small markets. Germany and the UK suffer from higher interest rates, postponing FTTH projects. However, in the UK market, Hexatronic has compensated for the downfall primarily with strong sales to a large customer.

Among the smaller regions, APAC (Rest of the World) grew by 34% y/y, beating our forecast of 21%, thanks to the acquisition of KNET and FTTH deliveries in Australia, and Sweden declined by 15% y/y following lower activity in FTTH and lower sales to mobile carriers.

We are somewhat surprised by the relatively strong Europe and soft North America, which suggests that Hexatronic’s FTTH offering is doing relatively well while BDI, the US conduit & pipe business, is having a harder time.

Source: Hexatronic

Hexatronic’s three most important markets, the US, UK and Germany, the so-called strategic growth markets, all have significantly lower FTTH/B penetration rates than Sweden. First, the number of households in the US, UK and Germany is ~42x the Swedish number. Second, the FTTH/B subscription penetration rates span from ~25% in the US to ~10% in the UK and Germany, compared to Sweden’s ~70%. Thus, there is a vast market to compete for in the strategic growth markets and considering the rapid growth seen in 2021 and onwards, we believe Hexatronic has a strong position in the markets.

While these markets experience a slowdown in FTTH/B investments due to cost inflation and high interest rates, we believe these markets will be important over the next ~8-10 years.

EBITA and Margins: EBITA Margin as Expected – In Line with Target Despite Negative Organic Growth

EBITA was SEK296m, corresponding to an EBITA margin of 15.4% (18.3). Our forecast was SEK305m and 15.4%, and the slight miss was due to somewhat softer sales. The slightly lower gross margin than expected was compensated for by solid cost control on OPEX. Thus, despite the negative organic growth, Hexatronic obtained an EBITA margin in line with its 15-17% target. Also, one-offs related to the carve-out acquisition, Rochester, impacted the EBITA margin negatively by 0.8% points in the quarter.

Source: Hexatronic

Cash Flow: NWC Relative to R12m Sales Remains High

The operating cash flow was SEK107m (255) and was negatively affected by a negative contribution from net working capital (NWC) of SEK113. NWC relative to rolling twelve months sales was 21.8%, in line with the level seen in H1 but higher than our estimate. We did expect a gradual improvement in H2, as seen in 2022. Nevertheless, there are positive signs, with inventory declining as a share of sales, which, however, was offset by declining accounts payable.

Source: Hexatronic

Acquisitions: USNet and ATG Technology

Since our last Update, Hexatronic has made two smaller acquisitions, USNet and ATG Technology.

USNet

“USNet is a US-based company that offers installation, project management, decommissioning, and relocation services nationwide for large-scale data center customers. The acquisition strengthens Hexatronic’s US data center position further through broader service offerings and with the possibility to provide cross-selling opportunities to both national and international clients together with Data Center Systems, a current company within Hexatronic Group. USNet today has 26 employees and an annual revenue of approximately 10 MUSD.

The US is Hexatronic’s largest market and one of the company’s strategic growth markets. The acquisition of USNet allows for additional diversification of Hexatronic’s business and increased opportunities within the growing market for data centers. Following the completion of the acquisition, Hexatronic’s data center business will increase to around 6-7 percent of annual group sales, on a proforma basis.”

ATG Technology

“ATG Technology Group Limited ("ATG”) is a unique player in the New Zealand fiber industry. This strategic acquisition foremost complements an existing subsidiary with operations in Australia (Optical Solutions Australia - OSA). The acquisition also further enriches Hexatronic's portfolio and expands Hexatronic’s presence in the New Zealand market where Hexatronic already has a subsidiary that delivers passive fiber optic system solutions and has its own local microduct production facility.

Spanning optical cable, fiber connectivity, hand tools, fusion splicers and test & measurement, ATG aligns with Hexatronic's growth roadmap as it serves as a complementary add-on to OSA, a current company within the Hexatronic umbrella with operations in Australia. OSA and ATG currently share a number of supply partners, with the acquisition expanding ATG’s range to include more of OSA's partners and technology solutions. ATG today has six employees and an annual revenue of approximately 3 MNZD.”

Our Comments

While both acquisitions are rather small – which we believe is reasonable as it makes sense to strengthen the balance sheet further rather than making big acquisitions – we believe both make sense from a strategic perspective. USNet strengthens the US Data Center offering by adding country-wide resources and exposure to larger customers to DCS’s production capabilities. ATG Technology enhances the exposure to the New Zeeland market, where Hexatronic has production facilities.

Estimate Revisions: 13-21% Cuts on 2024e

We make no notable adjustments to our 2023 forecasts but lower sales and EBITA for 2024 by 13% and 21%. While we believe the outlook for 2023 in the report aligns with the Trading Update from 22 September, we now expect a weaker market during 2024, which the Trading Update did not consider.

We expect sales to be in line with the level seen in Q3 2023 throughout 2024, with adjustments for acquisitions and seasonality and a minor improvement in H2 2024. That results in a 13% cut in our sales forecasts.

We assume margins are slightly below Hexatronic’s 15-17% EBITA margin target in 2024. We note that the target considers “over a business cycle” and that Hexatronic outperformed the target in H2 2022 and H1 2023. We forecast a 14.5% in EBITA margin for 2024.

We have somewhat reduced our growth and margin assumptions for the longer term. We expect an average organic growth rate of c9% and an average EBITA margin of 15.7% from 2025-2029. We believe the structural need for FTTH remains high in the strategic growth market, the US, the UK and Germany, among others.

| Estimate Revisions | ||||||

| Sales | FYE 2023 | Old | Change | FYE 2024 | Old | Change |

| Net Sales | 8334 | 8463 | -2% | 8458 | 9760 | -13% |

| Y/Y Growth (%) | 27% | 29% | 1% | 15% | ||

| Sweden | 718 | 730 | -2% | 720 | 745 | -3% |

| Growth y/y (SWE) | -11% | -10% | 0% | 2% | ||

| Rest of Europe | 3973 | 3856 | 3% | 4316 | 4481 | -4% |

| Growth y/y (EU) | 35% | 31% | 9% | 16% | ||

| North America | 2923 | 3193 | -8% | 2646 | 3809 | -31% |

| Growth y/y (NA) | 32% | 44% | -9% | 19% | ||

| Rest of the World | 722 | 684 | 5% | 777 | 725 | 7% |

| Growth y/y (RotW) | 18% | 12% | 8% | 6% | ||

| Other operating income | 89 | 75 | ||||

| Costs | ||||||

| Gross Profit | 3621 | 3739 | -3% | 3599 | 4295 | -16% |

| Gross Margin | 43.4% | 44.2% | 42.5% | 44.0% | ||

| OPEX | -2120 | -2203 | -4% | -2203 | -2557 | -14% |

| Growth y/y | 25.5% | 30.4% | 3.9% | 16.1% | ||

| Earnings | ||||||

| EBITA | 1371 | 1394 | -2% | 1230 | 1563 | -21% |

| EBITA Margin (%) | 16.4% | 16.5% | 14.5% | 16.0% | ||

| Diluted EPS | 4.10 | 4.26 | -4% | 3.66 | 5.02 | -27% |

| Forecasts | ||||||||

| Sales | Q1A 2023 | Q2A 2023 | Q3A 2023 | Q4E 2023 | FYE 2023 | FYE 2024 | FYE 2025 | FYE 2026 |

| Net Sales | 2115 | 2258 | 1917 | 2044 | 8334 | 8458 | 9182 | 10063 |

| Y/Y Growth (%) | 52% | 36% | 11% | 14% | 27% | 1% | 9% | 10% |

| Sweden | 178 | 176 | 165 | 199 | 718 | 720 | 734 | 749 |

| Growth y/y (SWE) | 15% | -28% | -15% | -8% | -11% | 0% | 2% | 2% |

| Rest of Europe | 998 | 1099 | 893 | 983 | 3973 | 4316 | 4661 | 5034 |

| Growth y/y (EU) | 55% | 47% | 19% | 23% | 35% | 9% | 8% | 8% |

| North America | 752 | 828 | 671 | 672 | 2923 | 2646 | 2963 | 3408 |

| Growth y/y (NA) | 73% | 58% | 4% | 10% | 32% | -9% | 12% | 15% |

| Rest of the World | 187 | 156 | 188 | 191 | 722 | 777 | 823 | 873 |

| Growth y/y (RotW) | 20% | 7% | 34% | 11% | 18% | 8% | 6% | 6% |

| Other operating income | 23 | 22 | 24 | 20 | 89 | 80 | 80 | 80 |

| Costs | ||||||||

| Gross Profit | 945 | 995 | 812 | 869 | 3621 | 3599 | 3948 | 4327 |

| Gross Margin | 44.7% | 44.1% | 42.4% | 42.5% | 43.4% | 42.5% | 43.0% | 43.0% |

| OPEX | -555 | -558 | -484 | -523 | -2120 | -2203 | -2387 | -2616 |

| Growth y/y | 49% | 37% | 15% | 7% | 25% | 4% | 8% | 10% |

| Other operating income | 23 | 22 | 24 | 20 | 89 | 80 | 80 | 80 |

| Earnings | ||||||||

| EBITA | 365 | 405 | 296 | 306 | 1371 | 1230 | 1399 | 1564 |

| EBITA Margin (%) | 17.3% | 17.9% | 15.4% | 15.0% | 16.4% | 14.5% | 15.2% | 15.5% |

| Diluted EPS | 1.09 | 1.27 | 0.85 | 0.91 | 4.10 | 3.66 | 4.31 | 4.93 |

Valuation

We lower our Base Case to SEK67 (87) following decreased sales and margin forecasts for 2024 and a raised WACC, as we increase our risk-free rate from 2.5% to 3%. Although we believe the market softness is temporary, as investments in FTTH remain important for underpenetrated countries, we now assume slightly lower growth rates and margins over the mid-and long run.

While the Bull Case assumes slightly higher growth and margins 2023-2030, the main difference is in the 2030-terminal period. Unlike our Base Case, where we expect the strategic growth markets to have negative sales growth from 2030 and onwards (like in Sweden post-2017), our Bull Case assumes flat sales and minor margin declines.

In our Bull Case, we expect Hexatronic to increase its sales from non-FTTH sources until 2030, fast enough to limit the expected downturn in FTTH. While Hexatronic has exposure to Harsh environment, core networks, 5G, farming, and data centres, most revenues are generated from FTTH. However, Hexatronic has a solid M&A track record, and several recent acquisitions, such as DCS, Weterings, Rochester, and Fibron, have added exposure to non-FTTH segments. Also, at least five-ten years are likely left until the FTTH boom is over in the strategic growth markets. Thus, Hexatronic has plenty of time to add additional sources of revenue until then, and M&A will likely play a major role.

Our Bear case assumes slightly lower growth and margins in 2023-2030. However, the major difference concerns the period after 2030. For example, our bear case assumes 5% in terminal EBIT margin compared to 9% in our base case. In the bear case, we believe the maturity of the current growth markets, the US, the UK and Germany, will significantly negatively impact growth and margins and that Hexatronic cannot offset the downturn with new markets or segments.

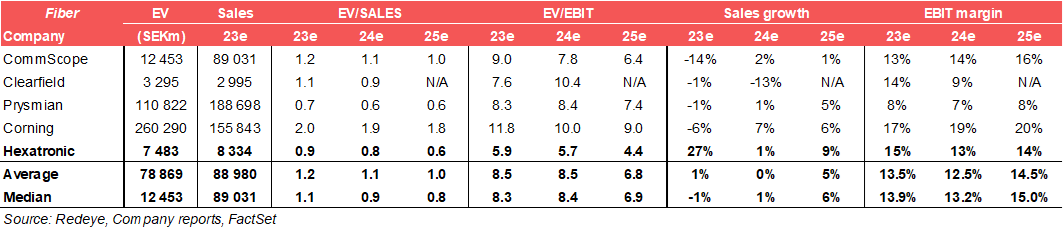

Peer Valuation

While most companies with exposure to FTTH and similar have seen their valuation multiples decline significantly, Hexatronic is trading at a discount to its peers. However, note that some peers are substantially larger than Hexatronic.

Investment thesis

Case

Pole position in the boom for digital highways.

Evidence

Proven track record in several major markets with its easy-deployed high-quality system solutions.

Challenge

Boom and bust FTTH cycle put risks to the very long-term.

Challenge

Possible price pressure.

Valuation

Base Case of SEK 67 implies ~13x EBITA 2024E

Quality Rating

People: 4

Hexatronic has a strong management team of entrepreneurial people with plenty of skin in the game. CEO has significant experience from the telecom industry. Staff at other key positions, that joined the group through last year's acquisitions, are also intact. The company has delivered so far on their financial goals.

Business: 4

Due to the competitive situation, product differentiation appears to be difficult, thus the price will always be an issue. Hexatronic is a small player compared to some of the dominant multinational companies. Surely that means growth opportunities but also challenges.

Financials: 4

In our view, Hexatronic is very financially stable and receives a good score in most subcategories. Overall we view Hexatronic's profitability levels as compelling and improving. We see some risks for new rights issues given the strong focus on acquisitions, still if the acquisition is done at good prices and creates value this will not be an issue.

Financials

| Income statement | |||||

| SEKm | 2020 | 2021 | 2022 | 2023e | 2024e |

| Revenues | 2,080.8 | 3,491.5 | 6,574.0 | 8,334.3 | 8,458.0 |

| Cost of Revenue | 1,142.9 | 1,957.6 | 3,704.6 | 4,713.5 | 4,859.2 |

| Operating Expenses | 660.1 | 1,041.7 | 1,633.5 | 2,031.3 | 2,123.1 |

| EBITDA | 277.8 | 492.2 | 1,235.9 | 1,589.5 | 1,475.7 |

| Depreciation | 68.7 | 95.6 | 145.6 | 218.8 | 246.0 |

| Amortizations | 27.5 | 38.7 | 62.3 | 110.0 | 116.0 |

| EBIT | 177.3 | 354.8 | 1,027.6 | 1,260.7 | 1,113.8 |

| Shares in Associates | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Interest Expenses | -12.4 | -23.1 | -68.1 | -120.1 | -148.3 |

| Net Financial Items | 12.4 | 23.2 | 125.1 | 121.1 | 148.3 |

| EBT | 164.9 | 331.7 | 1,029.1 | 1,141.6 | 965.4 |

| Income Tax Expenses | -37.9 | -79.8 | -223.7 | -298.7 | -212.4 |

| Net Income | 127.0 | 251.9 | 793.0 | 842.9 | 753.0 |

| Balance sheet | |||||

| Assets | |||||

| Non-current assets | |||||

| SEKm | 2020 | 2021 | 2022 | 2023e | 2024e |

| Property, Plant and Equipment (Net) | 441.1 | 1,071.9 | 1,629.7 | 2,441.5 | 2,421.2 |

| Goodwill | 257.2 | 1,064.5 | 2,490.8 | 3,089.0 | 3,089.0 |

| Intangible Assets | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Right-of-Use Assets | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Other Non-Current Assets | 293.2 | 322.5 | 3.8 | 6.0 | 6.0 |

| Total Non-Current Assets | 991.5 | 2,458.9 | 4,124.3 | 5,536.5 | 5,516.2 |

| Current assets | |||||

| SEKm | 2020 | 2021 | 2022 | 2023e | 2024e |

| Inventories | 410.3 | 928.8 | 1,596.1 | 1,708.5 | 1,860.8 |

| Accounts Receivable | 308.0 | 597.3 | 1,018.2 | 1,500.2 | 1,353.3 |

| Other Current Assets | 31.1 | 55.1 | 97.7 | 116.7 | 118.4 |

| Cash Equivalents | 212.2 | 675.1 | 552.0 | 840.8 | 1,926.7 |

| Total Current Assets | 961.6 | 2,256.3 | 3,264.0 | 4,166.2 | 5,259.2 |

| Total Assets | 1,953.1 | 4,715.2 | 7,388.3 | 9,702.7 | 10,775.4 |

| Equity and Liabilities | |||||

| Equity | |||||

| SEKm | 2020 | 2021 | 2022 | 2023e | 2024e |

| Non Controlling Interest | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Shareholder's Equity | 649.4 | 1,647.5 | 2,805.1 | 3,669.9 | 4,294.9 |

| Non-current liabilities | |||||

| SEKm | 2020 | 2021 | 2022 | 2023e | 2024e |

| Long Term Debt | 453.5 | 1,255.3 | 1,810.6 | 2,964.0 | 2,964.0 |

| Long Term Lease Liabilities | 0.00 | 332.4 | 371.8 | 510.0 | 510.0 |

| Other Non-Current Lease Liabilities | 167.8 | 104.8 | 642.3 | 676.0 | 676.0 |

| Total Non-Current Liabilities | 621.3 | 1,692.5 | 2,824.7 | 4,150.0 | 4,150.0 |

| Current liabilities | |||||

| SEKm | 2020 | 2021 | 2022 | 2023e | 2024e |

| Short Term Debt | 82.0 | 274.3 | 100.0 | 126.0 | 126.0 |

| Short Term Lease Liabilities | 41.3 | 61.4 | 68.0 | 89.0 | 89.0 |

| Accounts Payable | 526.3 | 721.0 | 1,138.9 | 1,208.5 | 1,522.4 |

| Other Current Liabilities | 74.0 | 318.4 | 451.7 | 458.4 | 592.1 |

| Total Current Liabilities | 723.6 | 1,375.1 | 1,758.6 | 1,881.9 | 2,329.5 |

| Total Liabilities and Equity | 1,994.4 | 4,715.1 | 7,388.4 | 9,701.7 | 10,774.4 |

| Cash flow | |||||

| SEKm | 2020 | 2021 | 2022 | 2023e | 2024e |

| Operating Cash Flow | 249.8 | 104.7 | 669.5 | 866.2 | 1,555.6 |

| Investing Cash Flow | -229.0 | -1,154.3 | -639.7 | -1,407.3 | -225.7 |

| Financing Cash Flow | 89.5 | 1,511.0 | 270.6 | 816.0 | -244.0 |

Rating definitions

The team

Disclosures and disclaimers

Contents

Review of Q3 2023

Sales: Negative Organic Growth Following Softer Market

EBITA and Margins: EBITA Margin as Expected – In Line with Target Despite Negative Organic Growth

Cash Flow: NWC Relative to R12m Sales Remains High

Acquisitions: USNet and ATG Technology

Estimate Revisions: 13-21% Cuts on 2024e

Valuation

Investment thesis

Quality Rating

Financials

Rating definitions

The team

Download article