Egetis: Licensing agreement opens the path to Japan

Research Update

2023-11-15

10:40

Redeye provides an additional comment on the recent news that Egetis has outlicensed the rights to Emcitate in Japan to Fujimoto. We argue that Egetis now has a credible strategy in Japan in place and see the deal as a confirmation of the merits of focusing on partnerships in regions beyond the US and EU.

FT

Fredrik Thor

Contents

Investment thesis

US ReTRIACt trial

Named patients program

Quality Rating

Financials

Rating definitions

The team

Download article

Regional deal for Japan with Fujimoto

Last Friday, it was announced that Egetis had outlicensed the Emcitate rights to the company Fujimoto in Japan. According to the release, Fujimoto has “a long track record of bringing therapeutic medicines for CNS diseases, Blood diseases, and Orphan diseases to patients in Japan”. The deal structure features a relatively modest milestone value of SEK 45 million but instead grants Egetis approximately one-third of the future revenue stream. Furthermore, Fujimoto will stand for the regulatory interactions and the remaining development program, which likely will be a relatively small clinical study in Japanese patients, similar to the ReTRIAc trial in the US, we guess. Overall, we think this is a relatively well-balanced deal for Egetis as the company does not need to handle the regulatory interactions or conduct the remaining trial but retains a good portion of the revenues compared to many other regional peer deals amongst Swedish companies, which is more important at this stage given that Egetis now is well capitalized following the recent private placement and loan agreement. We think that the share price reaction has been too modest so far given the increased potential, but believe that investors likely are focused on EU and US progress at this stage.

Prevalence and market opportunity

Looking at the market opportunity, Egetis also mentions in the recent release that “Iwayama et al. (Ref. 1) have reviewed the literature of MCT8 deficiency in Japan, and identified 36 already published cases. Kubota et al. (Ref. 2) in turn have conducted a nationwide survey of MCT8 deficiency and estimated there are over 60 cases with the disease in Japan, although this survey mainly asked questions to pediatric hospital facilities and did not survey adult departments.” The prevalence assumption for MCT8 deficiency is typically one male in every 70,000, leading to an estimated 900 patients in Japan. This suggests a diagnosis rate of under 10%, aligning with figures seen in both the US and EU. We argue that disease awareness and improving the diagnosis of MCT8 deficiency will be a key part of the commercialization of MTC8, and we thus think that it's good to have local presence in Japan that can prepare the market. Currently, Egetis states that no patient is treated with Emcitate in Japan, in contrast to 25 other countries where patients are treated in compassionate use programs.

Initial assumptions

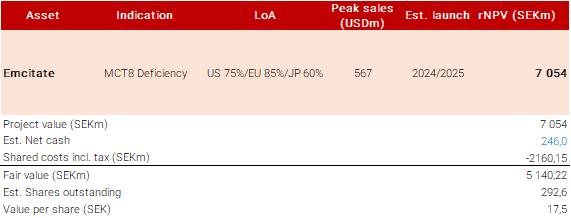

We know less about the regulatory path in Japan, but Egetis mentions that a local study is likely needed for regulatory approval. We think that this could mainly relate to a demand to study the drug candidate in a Japanese population, and likely that it could be similar in size to the now ongoing ReTRIACt trial in the US and look at T3 levels. We expect to learn more once further regulatory interactions have been conducted. In our initial assumptions, we estimate that a trial could be finalized sometime in 2025 and that an approval could be communicated in early/mid-2026. We have previously only included the US and EU in our market model but now see a good rationale to include Japan, following that a credible commercialization partner is in place. Given that we know less about the remaining regulatory path, we set a likelihood of approval at 60% currently compared to 85%/75% in the EU/US. We assume a price in line with our average EU price assumption of USD165000 per year. With these assumptions, we estimate a peak sale of some USD50m when assuming a peak diagnostics rate of 65% (same in US/EU) and that Emcitate takes around 45% of this patient population. This could very well be on the conservative side if all goes well, but we will adjust these assumptions more once we know more about the strategy and regulatory path for Japan. Overall, this leads to a raised base case to SEK17.5 (16) per share). We hope to dig a bit deeper into the market potential in Japan soon.

Key financials

| SEKm | 2021 | 2022 | 2023e | 2024e |

| Revenues | 38.2 | 22.6 | 35.0 | 96.2 |

| Revenue Growth | -7.3% | -40.9% | 54.9% | 175% |

| EBITDA | -103.6 | -195.4 | -283.0 | -283.4 |

| EBIT | -106.0 | -198.1 | -284.8 | -284.9 |

| Net Income | -104.9 | -193.8 | -283.8 | -283.9 |

Investment thesis

Case

De-risked orphan case at a discount

Evidence

Clear data on effectiveness supported by KOLs

Supportive Analysis

Challenge

Dependent on increased diagnoses

Challenge

In-house commercialisation requires strong team

Valuation

Unnecessarily cautious expectations priced into today’s share price

Emcitate

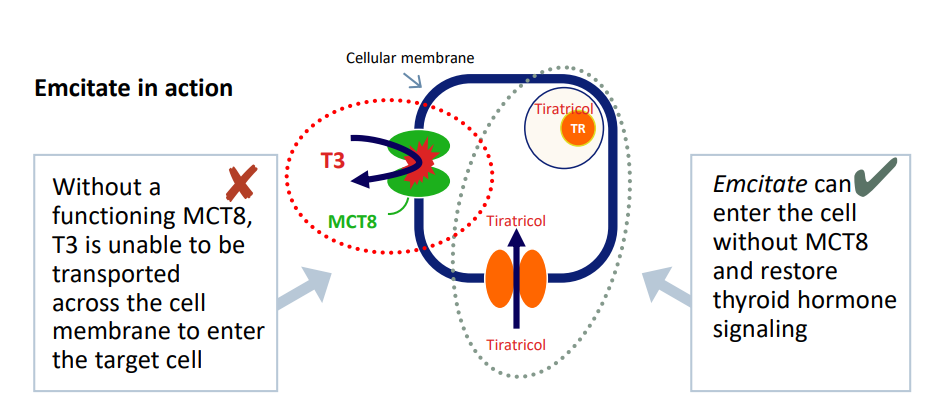

Emcitate, which contains the active substance tiratricol, does not require the MCT8 transporter to cross cell membranes and can mimic the activity of thyroid hormones by binding to thyroid hormone receptors in cells. In this way, tiratricol can bypass the deficiency of the MCT8 transporter and restore thyroid hormone signalling in the brain. The compound, a small molecule drug, has a favourable safety profile and has been used for more than 40 years in other indications. The drug candidate has most notably been tested in patients with MCT8 deficiency at the Erasmus Medical Center in Rotterdam, a leading research centre for this disease.

US ReTRIACt trial

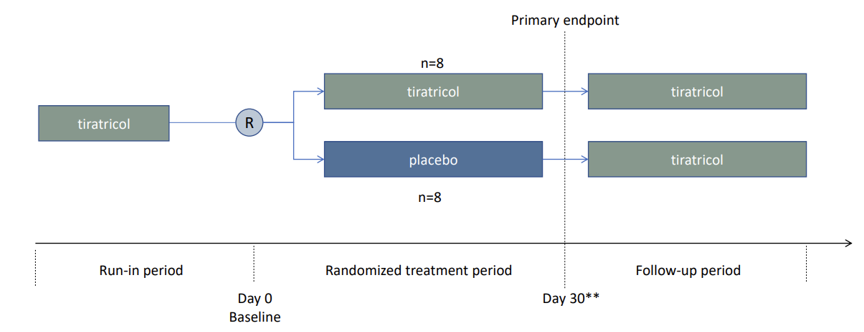

The remaining clinical step for Emcitate in the US is a small study (n=16), mainly patients in Egetis’s named patients programme, and the study aims to verify the effect on T3 levels over 30 days in a randomised setting. Compared to the previous trials, patients will already be on a stable dose of tiratricol (Emcitate) and will then be randomised to receive placebo or Emcitate for 30 days, or until reaching rescue criterion (T3 levels higher than the upper limit of normal of the participants’ normal range). All patients will again receive tiratricol in the follow-up period. The primary endpoint is the proportion of participants in the placebo group compared with the treatment group where the removal of Emcitate will lead to an increase of serum total T3 concentration above the upper limit of normal.

We conclude that Emcitate’s effect on T3 levels is well established, and the company cites data from nine patients in its named patients programme who were on “drug holiday”, i.e., temporarily off treatment, quickly returned to their high native serum T3 levels. The half-life of tiratricol is also 4–6 hours, leading to a quick response once off treatment. Overall, we see this as a relatively straightforward and low-risk trial.

Named patients program

Even though Emcitate has not yet been approved, 170 patients from over 25 counties have been supplied with Emcitate through “Named patient use”, a program that allows for early access to treatments in severe and life-threatening conditions. We note that growth has been steady and already results in a solid income stream, although the pricing is not close to what we expect it to be once an approved treatment. In Q4, Egetis announced that it had submitted a protocol for an expanded access program in the US, which will reduce the administration for early access to Emcitate before approval, to us an indication of the strong demand and also a good way to further pave the way for the commercial launch in 2024e. We think that converting named patients to fully reimbursed patients will be a key catalyst for sales growth at launch, given that these are identified and diagnosed patients known by Egetis. Our impression is that the conversion pace will depend on the country and specific rules regarding reimbursement. We expect a fast reimburment process in the US and countries like Germany and UK in Europe, and expect a transition process after approval and before national reimbursement to result in a pricing similar to that under the named patient program.

Quality Rating

People: 4

Egetis have a small but experienced executive management team. The ownership structure has changed significantly after the merger with Rare Thyroid Therapeutics. The largest shareholder Peder Walberg is an operative board member.

Business: 3

Egetis does not yet market any products. However, it is in late-stage clinical development. It targets attractive rare disease/niche markets where we see an above-average likelihood of approval, high pricing, and no competition from approved treatments.

Financials: 1

Egetis has no history of profitability but now has a strong cash position that should last beyond the sales of its priority review voucher.

Financials

| Income statement | |||

| SEKm | 2022 | 2023e | 2024e |

| Revenues | 22.6 | 35.0 | 96.2 |

| Cost of Revenue | 6.3 | 0.00 | 0.00 |

| Operating Expenses | 211.7 | 318.0 | 379.6 |

| EBITDA | -195.4 | -283.0 | -283.4 |

| Depreciation | 0.68 | 1.8 | 1.4 |

| Amortizations | 0.00 | 0.00 | 0.00 |

| EBIT | -198.1 | -284.8 | -284.9 |

| Shares in Associates | 404.8 | 404.8 | 404.8 |

| Interest Expenses | 0.70 | 1.0 | 1.0 |

| Net Financial Items | 4.3 | 1.0 | 1.0 |

| EBT | -193.8 | -283.8 | -283.9 |

| Income Tax Expenses | 0.00 | 0.00 | 0.00 |

| Net Income | -193.8 | -283.8 | -283.9 |

Rating definitions

The team

Disclosures and disclaimers

Contents

Investment thesis

US ReTRIACt trial

Named patients program

Quality Rating

Financials

Rating definitions

The team

Download article