Enviro Q3 2023: No drama

Research Update

2023-11-24

07:00

Redeye comments on Enviro’s Q3 report, which was very much on the same theme as we saw in Q2, where the preparatory work ahead of the final investment decision regarding the Uddevalla plant continued. We understand things are progressing according to plan, although it is taking longer than expected, but a final investment decision is approaching. As a result, we take a more conservative near-term view on the expected plant roll-out and also increase our WACC based on the current macroeconomic environment, which impacts our fair value range.

ME

Mattias Ehrenborg

Contents

Q3 wrap-up and an update on the Uddevalla investment decision

New product launch

Q3 financials

Estimate changes and Valuation - reduced fair value range on the back of reduced near-term estimates, leverage assumptions, and increased WACC

Investment thesis

Quality Rating

Financials

Rating definitions

The team

Download article

Q3 presented no drama

Enviro’s Q3 report was very similar to the Q2 report in terms of the quarter being dominated by work, planning, and preparations ahead of the final investment decision for the Uddevalla plant. This is the key event in the near term, as it will act as a catalyst for the construction of the plant. The Q3 figures themselves were largely in line with our estimates, and the cash position by the end of Q3 sits at SEK243m.

The final investment decision for Uddevalla is yet to come – we reduce our near-term estimates

The process ahead of the final investment decision (FID) has taken longer than we expected, which is also why we expect the plant to be up and running by H2 2025 rather than H1 2025 if we assume an FID in Q1 2024 (18 months construction time). Our previous estimates reflected a final investment decision in Q3, which did not happen. Therefore, we reduce our 2025 estimates and slightly postpone the timing of the following plant roll-out.

Reduced fair value range on the back of estimate changes and increased WACC

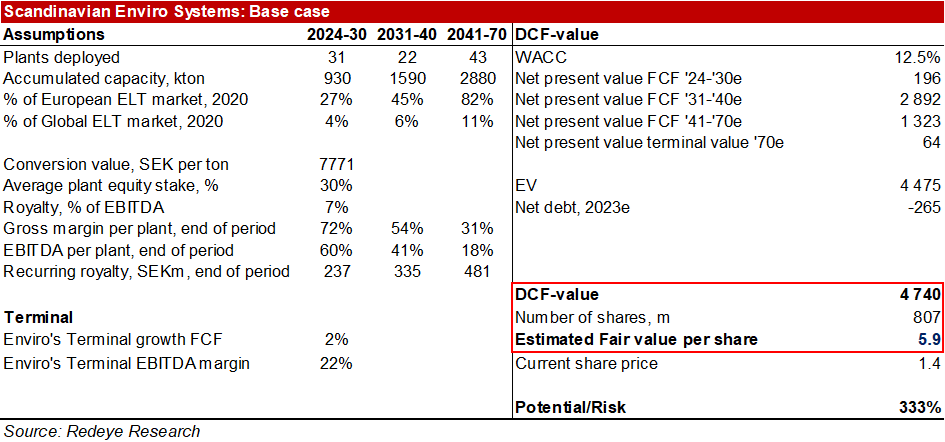

Given the current macroeconomic environment, we also reduce our leverage assumptions for the plants to take a more conservative approach. We have previously had 80% leverage in our estimates, which is high but not entirely unusual for infrastructure investments. We reduce this number to 60%, which is in line with typical project financing for wind farms (which we argue shares many similar investment characteristics) in this current macro environment. We also increase our WACC by 0.5pp to 12.5% on the back of Redeye increasing the interest rate by 0.5pp on all covered companies in its universe. All in all, our new fair value range sits at SEK1.1(2.1)-SEK11.1(11.1) with a base case of SEK5.9(6.1) per share.

Key financials

| SEKm | 2021 | 2022 | 2023e | 2024e | 2025e |

| Revenues | 8.6 | 7.7 | 63.0 | 58.8 | 66.1 |

| Revenue Growth | 353% | -10.7% | 722% | -6.6% | 12.3% |

| EBITDA | -43.5 | -69.8 | -24.0 | -32.4 | -31.2 |

| EBIT | -56.9 | -83.8 | -38.0 | -46.4 | -46.3 |

| EBIT Margin | -663% | -1094% | -60.4% | -78.9% | -70.2% |

| Net Income | -57.0 | -83.6 | -38.5 | -46.9 | -46.8 |

| EV/Revenue | 123 | 176 | 13.2 | 16.7 | 15.9 |

| EV/EBIT | -18.6 | -16.1 | -21.8 | -21.2 | -22.6 |

Q3 wrap-up and an update on the Uddevalla investment decision

As previously highlighted, we do not track the financial development closely until Enviro fully commercialises its business model and gets its first plant up and running. Instead, we monitor the operational development, news regarding plant talks, financing, and negotiations with relevant parties – such as potential customers and their production tests.

Enviro’s Q3 report was very similar to the Q2 report in terms of the quarter being dominated by work, planning, and preparations ahead of the final investment decision for the Uddevalla plant.

Thomas Sörensson states the following in the Q3 report: “Intense efforts have been underway ever since the announcement this spring, primarily with the intent of securing and performing quality assurance on all technical, commercial and legal parts that must be in place ahead of the construction of the Uddevalla plant, and also to lay the basis for the continued roll-out of forthcoming plants after the one being planned in Uddevalla. While the preparatory work has taken longer than we previously estimated, we are now nearing the point when the joint venture can make the final investment decision to then start construction of the plant in Uddevalla.”.

It is difficult to assess how near Enviro is to the point of making a final investment decision, but apart from the time component, which nonetheless is important, we understand things are progressing according to plan (which we find positive).

We have previously (in April 2023) expected a final investment decision to take place in Q2-Q3 2023, to revise it to Q3-Q4 in conjunction with the Q2 report in August, to now revising it to Q4-Q1. This clearly showcases how hard it is to predict the timing from an outside perspective and also that things have taken longer than expected.

However, we understand that a first-ever plant establishment of this character requires rigorous planning. Especially as every plant being rolled out after Uddevalle will use the same setup (in order to enjoy time and cost efficiency, which is needed for the roll-out and the financials of each plant). As such, we argue that getting it right from the start is very important.

We expect construction to take around 18 months, and we previously said that to have the plant up and running by the start of 2025, an investment decision was likely needed to be taken in Q3 2023 at the latest. It is also a possibility that construction might take longer than 18 months to complete since this is the first plant establishment Enviro will make. This is why the preparatory works are of great importance and also why we would rather see it taking an extra quarter to get in place rather than pushing it through too quickly. We now expect a FID by Q4-Q1, resulting in commercial operation by H2 2025.

Furthermore, Enviro’s Q2 report reiterated the target of having Uddevalla fully operational in 2025, but we have not found the same comment in this Q3 report. However, should the 2025 target not be relevant as of today, we believe the company would have highlighted this by now.

New product launch

Apart from the preparatory work related to Uddevalla, we note that Enviro has launched a new type of carbon black, developed on the basis of the feedback it has received from its customers. This was press released in October, but we still consider R&D efforts like this positive, as they increase the potential carbon black penetration in end-products and possibly the adoption rate.

Q3 financials

Enviro’s reported Q3 figures were all largely in line with our expectations. Sales amounted to SEK3.0m relative to SEK2.7m Q3 last year. We note that personnel costs have increased somewhat due to staff strengthening. All in all, EBIT amounted to SEK-20.7m relative to SEK-19.6m in Q3 2022, which is in line with what we expected.

We do not notice any compensation from the JV for historical costs that Enviro has historically invested. We believe that Enviro will receive this once a final investment decision has been made for Uddevalla.

Enviro’s cash position amounted to SEK243m by the end of the quarter, relative to SEK329m by the end of Q2 2023. The reason for this decrease is primarily due to a SEK40m amortisation of short-term debt that Enviro issued ahead of the directed share issue that took place in Q2 2023. Furthermore, Enviro generated a free cash flow of SEK-29m. We also note that cash flow expenses related to the share issue amounted to SEK-17m. In total, the net cash flow amounted to SEK-86m.

Estimate changes and Valuation - reduced fair value range on the back of reduced near-term estimates, leverage assumptions, and increased WACC

The Q3 report was largely in line with our expectations. However, given that the process ahead of the final investment decision (FID) has taken longer than we expected, we now expect the Uddevalla plant to be up and running by H2 2025 (instead of H1 2025) if we assume an FID in Q1 2024 (18 months construction time). Our previous estimates reflected a final investment decision in Q3, which did not happen. Therefore, we reduce our 2025 estimates and slightly postpone the following plant roll-out. For our bear case scenario, we take an even more conservative approach than in our base case, which is why the effect in this scenario is greater than in our other scenarios (which are kept rather intact).

We also reduce the expected debt-to-equity ratio for each plant going forward. We have previously had 80% leverage in our estimates, which is high but not entirely unusual for infrastructure investments. We reduce this number to 60%, which aligns with typical project financing for wind farms in this macro environment.

We also increase our WACC by 0.5pp (as Redeye has increased its risk-free rate on all covered companies). Due to this effect, our new fair value range sits at SEK1.1(2.1)-SEK11.1(11.1) with a base case of SEK5.9(6.1) per share. However, should the investment decision time increase significantly, there is further risk to our 2025 estimates and beyond.

All of our valuation scenarios are based on a successful launch of Uddevalla and the long-term roll-out of the following plants. We also expect all of the plants to be able to produce at full capacity and to sell their products largely at the rates Enviro has indicated in investor materials. Should the plants not produce at full capacity or sell their products at lower prices, there is a risk that the plants won’t be as profitable, which leaves a significant downside to our estimates and valuation if it were to play out.

This is a risk that is very difficult to assess here today, and we have not seen any signs until now that would imply this. However, this is something that we believe investors should be aware of.

The key catalyst we will be looking for going forward is the final investment decision regarding the Uddevalla plant, which we now expect will happen during Q4 or in Q1 at the latest. It is also in conjunction with the investment decision we expect Enviro to buy into the JV.

Investment thesis

Case

Offering a highly attractive solution for unsolved ELT recovery issue

Evidence

Michelin and Antin have validated Enviro and its technology

Challenge

Capital intensive business

Challenge

rCB fails to take off

Valuation

Significant upside potential but dependent on growth plan execution

Quality Rating

People: 4

Enviro has since 2001 developed its pyrolysis process, which evidently produces high-quality materials – which has been confirmed by Michelin and global oil companies. This gives us great belief in the people, as the founder is still active in the company (R&D manager) and CEO and CFO holds 5 years in their current positions, showcasing they can develop a technology to produce high-quality products. Furthermore, Enviro has attracted and successfully negotiated with Michelin, and is set to co-produce and co-own a production facility – a result of a demanding process that requires competences not often found in a relatively small organization as Enviro. However, given Enviro’s governance structure, a wide range of competencies can be found and utilized in the board of directors, in addition to management. Enviro is still in the inception of its commercialization phase, which makes it difficult to assess the track record of Enviro’s management, however, it looks solid to this date. To raise the score to a five, we would like to see a successful rollout of the commercialisation phase.

Business: 4

We believe Enviro is in an excellent position to benefit from several sustainability- and ESG trends in several markets. Enviro has a strong value proposition for customers and partners, offering raw materials with attractive sustainable characteristics with attractive margins and short payback times – whilst solving the environmental issue caused by ELTs. However, to this date, the business model is relatively unproven as Enviro is just entering its commercialisation phase, therefore scoring low in our rating system. However, future demand is expected to be very high, and we consider Enviro to possess several moats such as high product quality due to its patented pyrolysis process, and its partnership with Michelin, which we believe puts Enviro in the pole position.

Financials: 0

Enviro is now on the verge of fully commercializing its patented ELT pyrolysis technology. However, historical sales figures have been very low, and earnings deep in the reds – 2021 recorded a loss of SEK-57m. Without significant sales and so far, only negative earnings and cash flows, Enviro scores low in Financials category. We expect the company to rapidly grow sales over time from its current levels as plants are consecutively installed, while we also view additional funding necessary before break-even.

Financials

| Income statement | |||||

| SEKm | 2021 | 2022 | 2023e | 2024e | 2025e |

| Revenues | 8.6 | 7.7 | 63.0 | 58.8 | 66.1 |

| Cost of Revenue | 1.9 | 0.99 | 51.3 | 47.1 | 52.3 |

| Operating Expenses | -50.5 | -75.9 | -85.7 | -88.3 | -90.9 |

| EBITDA | -43.5 | -69.8 | -24.0 | -32.4 | -31.2 |

| Depreciation | -13.4 | -14.0 | -14.0 | -14.0 | -15.2 |

| Amortizations | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| EBIT | -56.9 | -83.8 | -38.0 | -46.4 | -46.3 |

| Shares in Associates | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Interest Expenses | 0.30 | 0.21 | 0.85 | 0.85 | 0.85 |

| Net Financial Items | -0.14 | 0.20 | -0.44 | -0.44 | -0.44 |

| EBT | -57.0 | -83.6 | -38.5 | -46.9 | -46.8 |

| Income Tax Expenses | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Net Income | -57.0 | -83.6 | -38.5 | -46.9 | -46.8 |

| Balance sheet | |||||

| Assets | |||||

| Non-current assets | |||||

| SEKm | 2021 | 2022 | 2023e | 2024e | 2025e |

| Property, Plant and Equipment (Net) | 70.7 | 78.8 | 71.0 | 183.1 | 181.4 |

| Goodwill | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Intangible Assets | 42.2 | 53.0 | 51.8 | 50.6 | 49.4 |

| Right-of-Use Assets | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Other Non-Current Assets | 0.15 | 0.00 | 0.00 | 0.00 | 0.00 |

| Total Non-Current Assets | 113.1 | 131.8 | 122.8 | 233.7 | 230.7 |

| Current assets | |||||

| SEKm | 2021 | 2022 | 2023e | 2024e | 2025e |

| Inventories | 2.3 | 2.1 | 3.5 | 4.1 | 5.0 |

| Accounts Receivable | 0.37 | 0.77 | 1.6 | 1.8 | 2.2 |

| Other Current Assets | 4.1 | 6.2 | 12.8 | 12.8 | 12.8 |

| Cash Equivalents | 123.2 | 30.0 | 286.7 | 130.7 | 66.8 |

| Total Current Assets | 130.0 | 39.0 | 304.6 | 149.4 | 86.7 |

| Total Assets | 243.0 | 170.8 | 427.4 | 383.2 | 317.5 |

| Equity and Liabilities | |||||

| Equity | |||||

| SEKm | 2021 | 2022 | 2023e | 2024e | 2025e |

| Non Controlling Interest | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Shareholder's Equity | 227.2 | 143.6 | 387.6 | 340.7 | 294.0 |

| Non-current liabilities | |||||

| SEKm | 2021 | 2022 | 2023e | 2024e | 2025e |

| Long Term Debt | 0.00 | 5.2 | 21.2 | 21.2 | 21.2 |

| Long Term Lease Liabilities | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Other Non-Current Lease Liabilities | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Total Non-Current Liabilities | 0.00 | 5.2 | 21.2 | 21.2 | 21.2 |

| Current liabilities | |||||

| SEKm | 2021 | 2022 | 2023e | 2024e | 2025e |

| Short Term Debt | 0.78 | 0.82 | 0.82 | 0.82 | 0.82 |

| Short Term Lease Liabilities | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Accounts Payable | 15.1 | 21.2 | 17.7 | 20.4 | 1.5 |

| Other Current Liabilities | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Total Current Liabilities | 15.9 | 22.1 | 18.5 | 21.2 | 2.3 |

| Total Liabilities and Equity | 243.0 | 170.8 | 427.4 | 383.2 | 317.5 |

| Cash flow | |||||

| SEKm | 2021 | 2022 | 2023e | 2024e | 2025e |

| Operating Cash Flow | -41.3 | -65.7 | -36.8 | -31.0 | -51.8 |

| Investing Cash Flow | -14.4 | -32.8 | -5.0 | -125.0 | -12.2 |

| Financing Cash Flow | 139.4 | 5.2 | 298.5 | 0.00 | 0.00 |

Rating definitions

The team

Disclosures and disclaimers

Contents

Q3 wrap-up and an update on the Uddevalla investment decision

New product launch

Q3 financials

Estimate changes and Valuation - reduced fair value range on the back of reduced near-term estimates, leverage assumptions, and increased WACC

Investment thesis

Quality Rating

Financials

Rating definitions

The team

Download article